-

Écrivez-nous

- Rapports phares

Parabolic Trough Collector Market Outlook Through 2035

Publié le 24 June, 2026

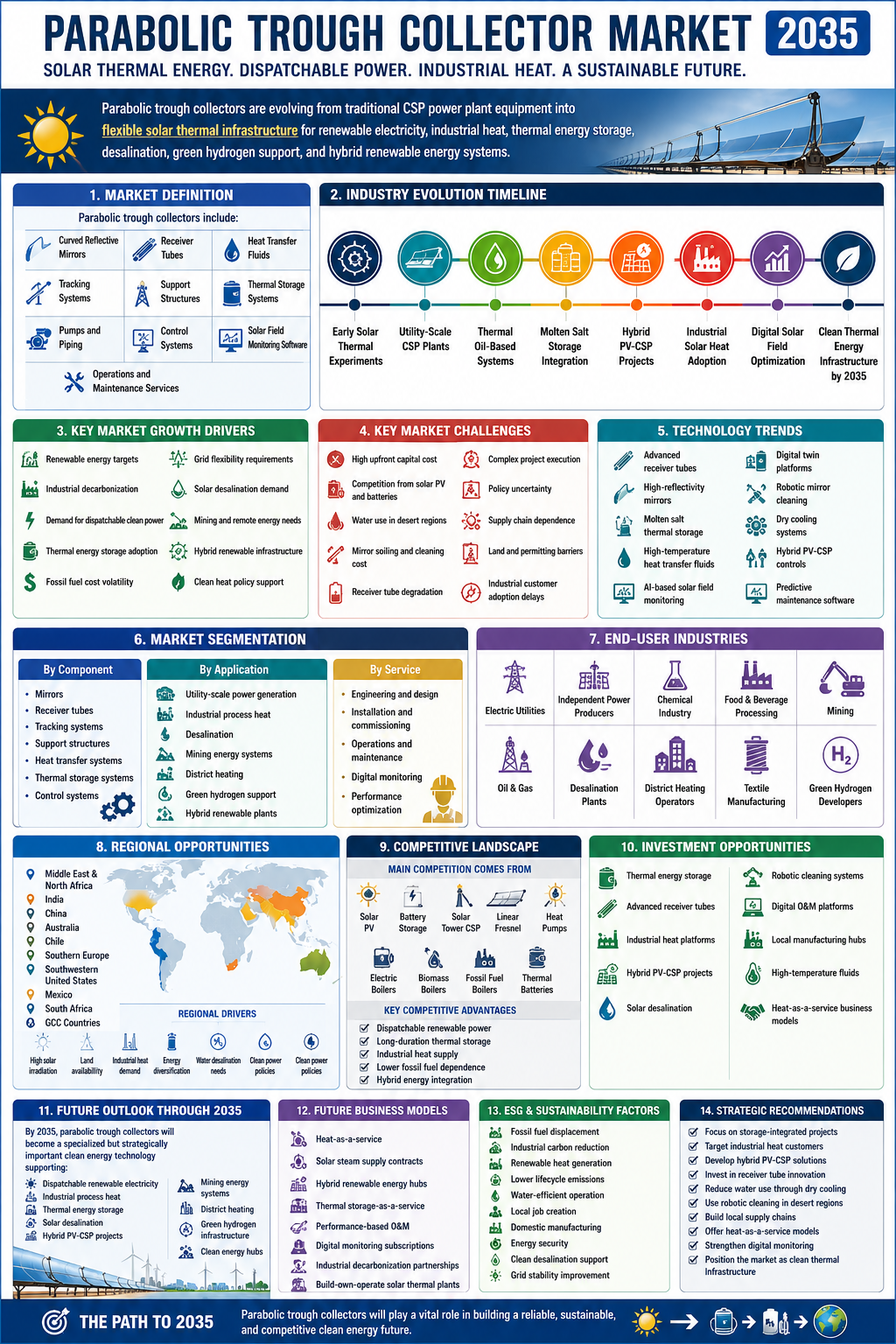

The Parabolic Trough Collector Market is positioned as one of the most important segments within concentrated solar thermal technology because it combines proven solar field engineering, dispatchable renewable power generation, industrial heat capability, and long-duration thermal energy storage integration. Unlike intermittent solar photovoltaic systems that primarily generate electricity when sunlight is available, parabolic trough collectors convert direct solar radiation into thermal energy that can be stored, dispatched, or used directly in industrial processes. Through 2035, the market is expected to evolve from a utility-scale power generation technology into a broader decarbonization platform serving electricity, process heat, hybrid renewable plants, green hydrogen, desalination, district heating, and energy-intensive industries.

The Parabolic Trough Collector Market is growing because governments, utilities, industrial users, and infrastructure investors are seeking renewable technologies that can provide heat, power, and storage flexibility. Demand is being shaped by energy security concerns, decarbonization targets, rising industrial electrification, grid reliability needs, and increasing interest in solar thermal systems that can complement solar PV and wind power.

Now Get Sample PDF Report on Global Parabolic Trough Collector Market Risk Analysis 2026-2033

https://www.statsndata.org/download-sample.php?id=296251

Key Takeaway

Parabolic trough collectors will remain strategically relevant through 2035 because they provide dispatchable solar thermal energy, not only daytime electricity.

Strategic Implication

For investors, developers, manufacturers, and policymakers, parabolic trough technology should be viewed as part of the next phase of renewable infrastructure, where storage, grid flexibility, and industrial heat decarbonization become as important as low-cost electricity generation.

The Parabolic Trough Collector Market refers to the global industry ecosystem involved in designing, manufacturing, installing, operating, and maintaining solar thermal collector systems that use curved reflective mirrors to concentrate direct sunlight onto linear receiver tubes. These receiver tubes carry a heat transfer fluid, which absorbs thermal energy and transfers it to a power block, thermal storage system, industrial process, or hybrid energy platform. The core market includes collector structures, mirrors, receiver tubes, tracking systems, heat transfer fluids, thermal storage equipment, control systems, engineering services, installation services, and operations and maintenance solutions.

Historically, parabolic trough technology has been one of the most commercially mature concentrated solar power technologies. Its adoption began in utility-scale solar thermal power plants and expanded in regions with high direct normal irradiation, large land availability, and policy support for renewable power. Over time, the technology has moved from basic oil-based heat transfer systems toward higher-temperature fluids, improved absorber coatings, advanced glass mirrors, automated cleaning systems, digital performance monitoring, and integration with molten salt thermal energy storage.

The strategic importance of parabolic trough collectors lies in their ability to address a key limitation of many renewable energy systems. Solar PV and wind power are low-cost and scalable, but they are variable. Parabolic trough systems can store heat and dispatch energy after sunset or during peak demand periods. This makes them valuable in markets where grid stability, evening peak power, industrial heat reliability, and fossil fuel displacement are policy priorities.

The current market landscape is shaped by a combination of opportunity and pressure. On one side, the global energy transition is creating demand for dispatchable renewable energy and industrial decarbonization. On the other side, parabolic trough systems face competition from falling solar PV costs, battery storage, solar tower CSP, and other clean energy technologies. The market therefore must compete not only on energy cost but also on reliability, storage duration, lifecycle value, heat quality, and integration flexibility.

Through 2035, the market is expected to become more specialized, more integrated, and more performance-driven. The strongest opportunities are likely to emerge where parabolic trough collectors are not treated as standalone solar assets but as part of larger energy systems. These include hybrid solar PV-CSP plants, thermal storage hubs, industrial steam supply platforms, solar desalination facilities, refinery decarbonization projects, mining energy systems, green hydrogen production, and district-scale thermal infrastructure.

Why It Matters

The market matters because global decarbonization requires renewable heat as well as renewable electricity. Parabolic trough collectors can serve both roles.

Business Impact

Companies that can lower installed costs, improve receiver efficiency, reduce maintenance requirements, and integrate thermal storage will be positioned for stronger long-term demand.

Future Outlook

By 2035, the market is likely to shift from traditional CSP power plants toward flexible solar thermal infrastructure serving utilities, industries, and hybrid renewable energy systems.

Market Ecosystem and Value Chain Analysis

The Parabolic Trough Collector Market operates through a complex value chain that connects raw material suppliers, precision component manufacturers, solar field integrators, engineering contractors, project developers, utilities, industrial users, financiers, and service providers. Value creation depends on how efficiently sunlight is converted into useful thermal energy, how reliably that heat is stored or delivered, and how effectively lifecycle costs are controlled. The ecosystem is capital-intensive, engineering-driven, and highly dependent on project execution quality. Through 2035, value will increasingly move toward integrated system providers that can combine solar field design, thermal storage, digital monitoring, hybrid plant integration, and long-term performance guarantees.

The parabolic trough value chain begins with glass, steel, aluminum, selective coatings, receiver tubes, tracking systems, heat transfer fluids, and control electronics. These inputs are transformed into solar collector assemblies, integrated into solar fields, connected to storage or power systems, and delivered to utilities or industrial end users.

Key Takeaway

The strongest value creation occurs when component quality, engineering design, project execution, and long-term operations are aligned.

Strategic Implication

Market participants should focus on supply chain reliability, local manufacturing partnerships, advanced components, and integrated service models to improve competitiveness.

The raw material foundation of the parabolic trough collector market includes low-iron glass for mirrors, steel and aluminum for support structures, stainless steel and specialty alloys for receiver tubes, selective absorber coatings, insulation materials, synthetic oils or molten salts for heat transfer, and electronic components for tracking and control systems. Each material influences performance, durability, cost, and maintenance requirements. Mirror quality determines optical efficiency. Receiver tube coatings influence heat absorption and thermal losses. Structural materials affect wind resistance, installation cost, and long-term field stability.

The component layer includes parabolic mirrors, absorber tubes, vacuum envelopes, bellows, support frames, pylons, hydraulic or electric tracking drives, sensors, control units, piping systems, pumps, expansion tanks, heat exchangers, and thermal storage equipment. Unlike modular solar PV panels, parabolic trough systems require precise mechanical alignment and thermal engineering. Small errors in mirror curvature, tracking accuracy, receiver positioning, or fluid circulation can reduce system performance. This makes engineering precision a central source of market value.

Manufacturing is divided between standardized component production and project-specific customization. Mirrors and receiver tubes require specialized industrial capabilities, while mounting structures and piping systems can often be localized. This creates opportunities for regional manufacturing in high-growth markets such as the Middle East, India, North Africa, Australia, Latin America, and parts of Southern Europe. Localization can reduce logistics costs, support domestic content requirements, and improve project bankability.

The distribution network is not retail-oriented. It is project-based and typically involves engineering, procurement, and construction firms, renewable energy developers, utility buyers, industrial energy users, government procurement agencies, and infrastructure investors. Large projects are often developed through tenders, power purchase agreements, public-private partnerships, or industrial heat supply contracts. Service providers play a major role because system performance depends heavily on mirror cleaning, receiver maintenance, tracking calibration, fluid management, thermal storage inspection, and digital monitoring.

End users include electric utilities, independent power producers, industrial manufacturers, oil and gas operators, mining companies, desalination plants, chemical producers, food processors, cement producers, district heating operators, and green hydrogen developers. Each end user has different requirements. Utilities prioritize dispatchable electricity and grid integration. Industrial users prioritize process heat reliability, steam quality, fuel substitution, and operating cost stability. Desalination and hydrogen users prioritize continuous thermal input and integration with storage.

Through 2035, the value chain is expected to become more resilient and regionally diversified. Developers will seek suppliers that can guarantee component life, performance, spare parts availability, and maintenance support. Digital twins, predictive maintenance, automated mirror washing, advanced receiver diagnostics, and energy management software will become increasingly important parts of the service ecosystem.

Why It Matters

A parabolic trough project succeeds only when the full value chain performs reliably across decades of operation.

Business Impact

Suppliers with proven components, local execution capability, and lifecycle service models will gain competitive advantage.

Future Outlook

By 2035, the market ecosystem will shift toward integrated solar thermal platforms rather than isolated collector supply.

Technology Landscape and Industry Innovation

Parabolic trough technology is evolving from a mature solar thermal design into a digitally optimized, storage-integrated, industrial energy platform. The core principle remains the same: curved mirrors concentrate sunlight onto receiver tubes carrying a heat transfer medium. However, innovation is changing almost every technical layer of the system, including mirror materials, absorber coatings, receiver vacuum durability, tracking accuracy, thermal fluids, molten salt integration, control systems, cleaning automation, and hybridization with solar PV, batteries, biomass, gas turbines, desalination units, and hydrogen systems. Through 2035, technology innovation will focus on higher operating temperatures, lower thermal losses, lower water use, better storage economics, and improved lifecycle reliability.

Key technologies reshaping the market include advanced receiver tubes, high-reflectivity mirrors, molten salt heat transfer, synthetic oil alternatives, thermal energy storage, digital monitoring, robotic cleaning, predictive maintenance, and hybrid renewable control platforms.

Key Takeaway

The future of parabolic trough collectors depends on improving thermal efficiency, reducing operating cost, and integrating storage more effectively.

Strategic Implication

Technology providers should prioritize high-temperature operation, digital performance optimization, storage compatibility, and industrial heat applications.

The core technology of a parabolic trough collector is based on solar concentration. Long, curved mirrors follow the sun and focus direct solar radiation onto a linear receiver tube located at the focal line of the collector. A heat transfer fluid flows through the receiver tube and absorbs heat. That heat can be used to generate steam for a turbine, charge a thermal storage system, supply industrial heat, support desalination, or feed hybrid energy systems. The technology works best in areas with strong direct normal irradiation, clear skies, and available land.

The receiver tube is one of the most critical technology components. It typically includes an absorber pipe with selective coating, a glass envelope, vacuum insulation, and expansion joints. Its role is to absorb as much solar radiation as possible while minimizing heat loss. Future improvements in selective coatings, vacuum stability, anti-reflective glass, and high-temperature materials will directly improve system performance.

Heat transfer fluid technology is another major innovation area. Traditional parabolic trough systems often used synthetic thermal oil, which limited operating temperatures. Higher-temperature fluids, molten salts, particles, and alternative thermal media are being explored to increase efficiency and reduce storage costs. Molten salt integration is especially important because it can enable higher thermal storage capacity and longer dispatch duration.

Digital transformation is becoming a major performance lever. Solar field control software can optimize collector tracking, detect underperforming loops, monitor receiver degradation, predict pump failures, schedule cleaning, and manage energy dispatch. Artificial intelligence and machine learning can improve performance forecasting by combining weather data, mirror reflectivity data, heat transfer fluid temperature data, and power block operating data.

Product evolution is also visible in structural design. Lighter support structures, improved wind resistance, easier installation, modular collector assemblies, and automated alignment tools can reduce project cost and construction time. Robotic cleaning is gaining importance in desert environments where dust and sand can reduce mirror reflectivity. Water-efficient cleaning systems will become increasingly important in dry regions.

Through 2035, the technology roadmap will likely move in five directions. First, higher operating temperatures will improve power cycle efficiency and industrial process compatibility. Second, thermal storage integration will become standard in utility-scale applications. Third, hybrid PV-CSP systems will become more common because PV can deliver low-cost daytime electricity while parabolic trough systems provide stored thermal energy for evening demand. Fourth, industrial heat applications will expand as companies seek alternatives to natural gas and fuel oil. Fifth, digital lifecycle management will become a standard requirement for project financing and performance guarantees.

Why It Matters

Technology innovation determines whether parabolic trough systems can remain competitive in a rapidly changing renewable energy market.

Business Impact

Companies that improve efficiency and reduce lifecycle cost will be better positioned to win utility and industrial projects.

Future Outlook

By 2035, parabolic trough collectors will be more digital, more storage-oriented, and more integrated with industrial energy systems.

Major Growth Drivers

The Parabolic Trough Collector Market is being driven by the intersection of renewable energy growth, industrial decarbonization, energy security, grid flexibility, and long-duration storage demand. While solar PV dominates low-cost daytime electricity generation, parabolic trough collectors offer a different value proposition: they generate heat that can be stored and dispatched. This makes them relevant for markets that need renewable power beyond daylight hours, high-temperature process heat, fuel substitution, and stable energy supply. Through 2035, growth will be strongest where policy support, high solar irradiation, industrial heat demand, and infrastructure financing converge.

Market growth is driven by renewable energy targets, demand for dispatchable clean power, industrial heat decarbonization, energy security concerns, thermal storage integration, and investment in hybrid renewable infrastructure.

Key Takeaway

The strongest driver is not solar generation alone, but the need for renewable energy that is controllable, storable, and useful for heat-intensive applications.

Strategic Implication

Stakeholders should position parabolic trough collectors as flexible thermal infrastructure rather than only as electricity-generation equipment.

Economic drivers are central to the market outlook. Countries with high fossil fuel import dependence are seeking domestic renewable energy sources that reduce exposure to fuel price volatility. Parabolic trough systems can convert local solar resources into electricity or heat, reducing long-term operating cost uncertainty. For industrial users, the ability to replace natural gas, diesel, or fuel oil with solar thermal heat can improve cost stability and reduce carbon exposure.

Industry demand drivers are also expanding. Energy-intensive sectors such as chemicals, food processing, mining, textiles, refineries, metals, and desalination require large volumes of heat. Many of these applications cannot be fully decarbonized through electricity alone without major process redesign. Parabolic trough collectors can supply medium-temperature heat and steam, making them relevant for direct industrial decarbonization.

Government support remains a critical growth factor. Renewable energy targets, carbon pricing, clean heat policies, green industrial incentives, grid modernization programs, and public infrastructure funding can improve project economics. In regions with strong direct solar resources, governments are increasingly evaluating solar thermal energy as part of energy diversification strategies.

Infrastructure development also supports demand. New renewable energy zones, transmission corridors, industrial parks, desalination complexes, mining operations, and hydrogen hubs can create demand for large-scale solar thermal systems. Parabolic trough projects are particularly attractive where land availability, solar radiation, water management, and grid connection can be planned together.

Technology advancement is another major driver. Improved receiver tubes, higher-reflectivity mirrors, molten salt storage, advanced tracking systems, and digital performance management can reduce levelized energy costs and increase reliability. As system efficiency improves, parabolic trough collectors can compete more effectively in applications where dispatchability and heat value are rewarded.

The rise of hybrid energy systems will also stimulate demand. Solar PV may provide low-cost electricity during the day, while parabolic trough systems provide thermal storage and evening power. Batteries may handle short-duration balancing, while thermal storage supports longer-duration supply. This combination can reduce curtailment, improve renewable utilization, and support grid stability.

Through 2035, the market will be shaped by countries and industries that recognize the economic value of heat. Electricity-focused policies alone may not fully unlock the market. Clean heat mandates, industrial carbon reduction programs, green fuel strategies, and long-duration storage incentives will be more powerful demand accelerators.

Why It Matters

The global energy transition cannot succeed through electricity generation alone. Industrial heat must also decarbonize.

Business Impact

Developers that target industrial heat and hybrid infrastructure may find stronger commercial opportunities than those relying only on utility power markets.

Future Outlook

By 2035, growth will be strongest in regions with high solar resources, strong policy support, and large industrial heat demand.

Market Challenges and Risk Factors

Despite its strategic value, the Parabolic Trough Collector Market faces significant challenges related to capital intensity, project complexity, competition from solar PV and batteries, supply chain specialization, financing risk, land and water constraints, and operational reliability. Parabolic trough systems require precise engineering, long development timelines, strong solar resources, and disciplined maintenance. These factors can make projects more complex than modular solar PV installations. Through 2035, the market’s success will depend on reducing installed costs, improving bankability, strengthening supply chains, and proving value in applications where thermal storage and process heat provide measurable advantages.

The main risks include high upfront capital cost, technical complexity, competition from other renewables, supply chain bottlenecks, policy uncertainty, water use concerns, receiver degradation, mirror soiling, and project execution delays.

Key Takeaway

Parabolic trough technology must compete on total system value, not only on electricity cost.

Strategic Implication

Market participants should reduce risk through modular design, performance guarantees, digital monitoring, local supply chains, and targeted applications.

Operational risks are important because parabolic trough systems involve moving parts, high temperatures, thermal fluids, mirrors, pumps, receivers, and storage systems. Tracking systems must remain accurate, mirrors must remain clean, receiver tubes must maintain vacuum integrity, and heat transfer fluid must operate within safe temperature limits. Poor maintenance can reduce output and damage project economics.

Supply chain vulnerability is another challenge. Receiver tubes, specialized mirrors, selective coatings, tracking drives, thermal fluids, and molten salt equipment require qualified suppliers. If a project depends on imported components, currency fluctuations, logistics delays, tariffs, and geopolitical disruptions can increase cost. Local manufacturing can reduce risk, but only if quality standards are maintained.

Regulatory barriers can delay projects. Large solar thermal plants require land approvals, environmental permits, grid connection agreements, water access permissions, financing approvals, and often public procurement processes. Industrial heat projects may also require integration with factory operations, safety approvals, and process redesign.

Cost pressure is one of the most visible challenges. Solar PV and battery storage have become highly competitive, forcing parabolic trough projects to justify their higher complexity. However, this comparison is not always direct. PV produces electricity, while parabolic trough systems produce heat that can be stored or used for thermal applications. The market challenge is to clearly communicate and monetize this difference.

Competitive risks are increasing from solar towers, linear Fresnel systems, electric boilers, heat pumps, biomass boilers, green hydrogen boilers, thermal batteries, and grid-scale battery systems. Each competing technology has different strengths. Parabolic trough collectors must therefore focus on applications where their proven reliability, medium-temperature heat capability, and storage integration offer superior lifecycle value.

Technology adoption barriers also exist. Many industrial buyers are unfamiliar with solar thermal procurement, heat purchase agreements, thermal storage economics, and long-term performance modeling. This slows adoption compared with familiar fossil fuel boilers or modular PV systems. Developers must provide clear financial models, operational guarantees, and integration support.

Water use is another concern, especially in desert regions where CSP resources are strongest. Wet cooling can increase water demand, while dry cooling can increase cost and reduce efficiency. Advanced cleaning systems and dry cooling strategies are therefore essential for future projects.

Why It Matters

Market risks can weaken investor confidence if not managed through proven design, reliable suppliers, and disciplined operations.

Business Impact

Companies that reduce complexity and improve bankability will win stronger support from utilities, industrial users, and financiers.

Future Outlook

By 2035, successful projects will likely be those that combine thermal storage, digital monitoring, hybrid energy integration, and strong operations discipline.

Industry Trends Reshaping the Market

The Parabolic Trough Collector Market is being reshaped by several structural trends: the shift from electricity-only CSP toward renewable heat platforms, integration with molten salt storage, hybridization with solar PV, growth of industrial decarbonization, digitalization of solar field operations, and rising demand for dispatchable renewable infrastructure. These trends are changing the market’s identity. Parabolic trough collectors are no longer evaluated only as solar power plant components. They are increasingly viewed as flexible energy assets that can support clean heat, grid stability, fuel displacement, and long-duration storage. Through 2035, the most competitive players will align their offerings with this broader energy transition role.

Major trends include hybrid CSP-PV projects, thermal storage integration, industrial heat adoption, higher-temperature fluids, digital performance management, local manufacturing, water-efficient operations, and new project financing models.

Key Takeaway

The market is shifting from standalone CSP plants toward integrated solar thermal energy systems.

Strategic Implication

Businesses should reposition parabolic trough collectors around storage, heat, flexibility, and decarbonization value.

One of the most important trends is the move toward hybrid renewable energy systems. Solar PV provides low-cost electricity during daylight hours, while parabolic trough collectors can provide heat and stored energy for evening or industrial use. This hybrid model improves asset utilization and helps renewable projects deliver more stable output profiles.

Thermal energy storage is becoming central to market positioning. Without storage, parabolic trough systems may struggle to compete with solar PV. With storage, they can provide dispatchable renewable power, industrial heat buffering, and grid flexibility. Molten salt and other thermal storage media will therefore become increasingly important.

Industrial heat decarbonization is another major trend. Many industrial processes require heat rather than electricity. As companies face carbon reduction targets, they are exploring solar thermal systems to reduce fossil fuel use. Parabolic trough collectors are well suited for medium-temperature heat applications, making them relevant for food processing, textiles, chemicals, mining, desalination, and district heating.

Digital transformation is reshaping operations. Sensors, drones, thermal imaging, artificial intelligence, weather forecasting, mirror reflectivity monitoring, and predictive maintenance platforms can improve performance. Digital tools help operators identify underperforming collector rows, receiver tube degradation, tracking errors, pump inefficiencies, and cleaning needs.

Another trend is localization of supply chains. Governments and developers increasingly want domestic manufacturing, local jobs, and lower import dependence. Parabolic trough systems offer localization opportunities in steel structures, assembly, installation, operations, and maintenance, even if specialized receivers and coatings remain globally sourced.

Water-efficient design is gaining importance. Many high-solar-resource regions are water-stressed. Future projects will need dry cooling, low-water cleaning systems, robotic mirror cleaning, and improved dust management.

Customer behavior is also changing. Utilities are no longer purchasing only the cheapest daytime electricity. They increasingly need grid support, evening power, capacity value, and storage. Industrial customers are evaluating carbon exposure, fuel security, and long-term heat contracts. These shifts support parabolic trough systems when their value is properly structured.

Why It Matters

The market’s future depends on adapting to new renewable energy priorities beyond simple electricity generation.

Business Impact

Companies that offer hybrid, storage-enabled, and industrial heat solutions will capture higher-value opportunities.

Future Outlook

By 2035, parabolic trough collectors will be increasingly deployed as part of integrated clean energy systems rather than isolated CSP assets.

Product and Service Segment Analysis

The Parabolic Trough Collector Market includes physical equipment, integrated systems, engineering services, operations services, digital platforms, and lifecycle support solutions. Product segmentation is expanding as the market shifts from traditional utility-scale collectors toward industrial solar heat systems, hybrid renewable plants, modular collector fields, advanced receiver technologies, and thermal storage-integrated platforms. Service revenue is also becoming more important because long-term performance depends on maintenance, cleaning, monitoring, calibration, and component replacement. Through 2035, the most attractive segments will be those that improve lifecycle efficiency, reduce operating cost, and support project bankability.

Major segments include collector assemblies, mirrors, receiver tubes, tracking systems, support structures, heat transfer systems, thermal storage systems, control software, engineering services, installation services, operations and maintenance, and digital monitoring platforms.

Key Takeaway

The market is moving from hardware supply toward integrated lifecycle solutions.

Strategic Implication

Companies should combine product innovation with service contracts, digital tools, and performance-based business models.

The largest physical product category is the collector assembly, which includes parabolic mirrors, receiver tubes, support structures, tracking mechanisms, and mounting systems. This segment represents the visible solar field and directly determines energy capture efficiency. Improvements in mirror reflectivity, structure durability, tracking precision, and receiver performance can significantly affect output.

Receiver tubes are a high-value segment because they influence thermal efficiency and operating temperature. Advanced coatings, vacuum stability, corrosion resistance, and thermal durability are key differentiators. Replacement demand also creates recurring revenue because receiver tubes may require maintenance or replacement during a plant’s operating life.

Tracking systems are another important segment. Accurate solar tracking ensures that reflected sunlight remains focused on the receiver tube. Electric drives, hydraulic systems, sensors, and control software all contribute to performance. Future tracking systems will increasingly use digital calibration, automated fault detection, and predictive maintenance.

Heat transfer systems include thermal oils, molten salts, pumps, piping, valves, expansion tanks, heat exchangers, and control systems. This segment is becoming more strategic as higher-temperature operation and storage integration become priorities. Thermal storage systems represent one of the highest-growth opportunities because they convert solar heat into dispatchable energy.

Service segments include feasibility studies, solar resource assessment, engineering design, procurement, construction, commissioning, operations, maintenance, cleaning, performance monitoring, and asset management. Services are important because parabolic trough systems require long-term care. Poor cleaning, tracking errors, receiver degradation, or fluid issues can reduce performance.

Application segments include utility-scale power generation, industrial process heat, enhanced oil recovery, desalination, district heating, food processing, mining, chemical production, hydrogen production, and hybrid renewable systems. Utility-scale power remains important, but industrial heat is likely to grow faster because many industrial users need alternatives to fossil fuel boilers.

Revenue contribution varies by project type. Large CSP plants generate significant equipment and engineering revenue but require long development timelines. Industrial heat systems may be smaller but can scale across many facilities. Digital and O&M services provide recurring revenue and improve customer retention.

Emerging segment opportunities include modular industrial solar heat systems, solar steam-as-a-service, thermal energy storage retrofit packages, hybrid PV-CSP control systems, AI-based solar field optimization, and dry-region cleaning robotics.

Why It Matters

Product and service segmentation determines where companies can capture margin and build recurring revenue.

Business Impact

Firms that move beyond equipment sales into lifecycle performance services will gain stronger customer relationships.

Future Outlook

By 2035, service, software, storage, and industrial heat solutions will represent a larger share of market value.

End-User Industry Analysis

End-user demand for parabolic trough collectors is broadening from utilities to industrial energy consumers. Utilities value dispatchable renewable power and storage. Industrial users value renewable heat, steam generation, fuel cost stability, and carbon reduction. Desalination plants, mining sites, chemical producers, food processors, refineries, district heating systems, and emerging hydrogen producers are all potential demand centers. Through 2035, end-user growth will depend on whether parabolic trough systems can be integrated into real operating environments without disrupting production, increasing energy risk, or creating excessive capital burden.

Key end users include electric utilities, independent power producers, industrial manufacturers, mining operators, desalination facilities, chemical companies, food processors, district heating operators, refineries, and green hydrogen developers.

Industrial heat users may become one of the most important growth segments through 2035.

Strategic Implication

Market participants should tailor solutions to end-user heat profiles, reliability needs, carbon targets, and financing constraints.

Electric utilities and independent power producers remain major end users because parabolic trough systems can generate electricity from solar heat. When paired with thermal storage, these plants can deliver power after sunset, support evening peak demand, and improve grid reliability. This is valuable in markets with high solar PV penetration, where daytime electricity may become abundant but evening supply remains constrained.

Industrial manufacturers represent a major opportunity. Many industries use steam or thermal energy for drying, washing, cooking, chemical reactions, mineral processing, sterilization, and heating. Parabolic trough collectors can supply medium-temperature heat that replaces fossil fuels in selected processes. Food and beverage plants, textile mills, paper mills, chemical facilities, and pharmaceutical producers can benefit where solar resources and land availability are suitable.

Mining operations are another attractive end-user segment, particularly in remote regions with high solar irradiation and costly fuel logistics. Mines often require electricity, process heat, and water treatment. Solar thermal systems can reduce diesel dependence and improve energy security.

Desalination is a strategic application in water-stressed regions. Parabolic trough collectors can provide thermal energy for desalination processes or power for reverse osmosis when integrated into hybrid systems. Countries in the Middle East, North Africa, and parts of Asia-Pacific may evaluate solar thermal desalination as part of long-term water security planning.

Refineries and oilfield operations may use parabolic trough systems for steam generation, process heat, and fossil fuel displacement. While long-term oil demand may evolve, existing facilities remain large heat consumers and may adopt solar thermal systems to reduce emissions intensity.

District heating and cooling networks offer another opportunity, especially where cities are developing low-carbon thermal infrastructure. Parabolic trough systems can supply heat during sunny periods and charge seasonal or daily thermal storage systems.

Green hydrogen production could become a longer-term opportunity. While electrolyzers primarily require electricity, solar thermal systems may support high-temperature processes, water treatment, hybrid energy hubs, or future thermochemical hydrogen pathways.

End-user adoption patterns differ significantly. Utilities often procure through tenders and long-term contracts. Industrial users prefer energy service models, heat purchase agreements, or performance-based contracts that reduce upfront capital burden. This creates opportunities for developers that can finance, own, and operate solar thermal systems on behalf of customers.

Why It Matters

End-user diversification reduces dependence on utility-scale CSP projects and creates broader market resilience.

Business Impact

Suppliers that understand industrial heat requirements will unlock new commercial opportunities.

Future Outlook

By 2035, industrial heat, desalination, mining, and hybrid renewable hubs will represent a larger share of demand.

Competitive Environment and Strategic Positioning

The competitive environment in the Parabolic Trough Collector Market is shaped by engineering capability, component quality, project execution experience, cost competitiveness, technology integration, financing credibility, and long-term service capability. Competition is not limited to other parabolic trough suppliers. The market also competes with solar PV, battery storage, solar tower CSP, linear Fresnel systems, biomass heat, electric boilers, heat pumps, fossil fuel boilers, and emerging thermal storage technologies. Through 2035, strategic positioning will depend on proving where parabolic trough systems deliver superior value: dispatchable renewable power, industrial process heat, long-duration storage, and hybrid energy integration.

Competitive advantage depends on optical efficiency, receiver performance, installed cost, thermal storage integration, EPC capability, bankability, local supply chains, digital monitoring, and lifecycle service quality.

Key Takeaway

The market will reward integrated solution providers rather than standalone hardware suppliers.

Strategic Implication

Companies should differentiate through reliability, storage integration, industrial use-case expertise, and long-term performance guarantees.

The industry structure includes component manufacturers, solar field designers, EPC contractors, renewable project developers, utilities, industrial energy service providers, storage technology firms, and digital performance companies. Some companies specialize in mirrors, receiver tubes, tracking systems, or engineering services, while others provide integrated CSP solutions.

Competitive intensity is high because parabolic trough technology operates within a broader clean energy market where alternatives are rapidly improving. Solar PV and batteries are the strongest competitive reference points for electricity generation, while heat pumps, electric boilers, biomass, and thermal batteries compete in industrial heat. Parabolic trough systems must therefore focus on applications where direct solar heat and thermal storage offer clear advantages.

Differentiation strategies include higher thermal efficiency, lower installed cost, advanced receiver durability, modular construction, reduced water use, automated cleaning, integrated molten salt storage, hybrid PV-CSP design, and digital performance optimization. Project developers may also differentiate through financing structures such as build-own-operate models, heat-as-a-service contracts, and long-term energy service agreements.

Partnerships are increasingly important. Equipment suppliers may partner with EPC firms, utilities, industrial companies, storage providers, digital software firms, and infrastructure investors. Local partnerships can support permitting, construction, labor management, and domestic content requirements.

Market positioning should avoid presenting parabolic trough systems as a direct replacement for solar PV in all situations. Instead, the strongest positioning is as dispatchable solar thermal infrastructure, renewable industrial heat supply, and long-duration energy storage integration. This framing better reflects the technology’s strengths.

Competitive advantages will increasingly depend on bankability. Investors and customers want proven performance, warranties, spare parts availability, operations support, and predictable lifecycle economics. Companies with operating references, strong balance sheets, and reliable supply chains will have an advantage.

By 2035, the competitive landscape may consolidate around players capable of delivering integrated solar thermal projects with storage and digital asset management. Smaller component firms may survive by specializing in high-value technologies such as receiver tubes, coatings, tracking controls, robotic cleaning, and thermal performance analytics.

Why It Matters

Strategic positioning determines whether parabolic trough collectors are seen as outdated CSP hardware or valuable clean heat infrastructure.

Business Impact

Companies that communicate total system value will compete more effectively against lower-cost renewable alternatives.

Future Outlook

By 2035, competition will favor integrated, bankable, storage-enabled, and industrially focused solution providers.

Regional Market Analysis

Regional demand for parabolic trough collectors is closely tied to solar resource quality, land availability, energy policy, industrial heat demand, grid flexibility needs, fossil fuel import exposure, and infrastructure financing capacity. The strongest opportunities are expected in sun-rich regions with high direct normal irradiation, including the Middle East, North Africa, India, Australia, Southern Europe, parts of China, Latin America, and the southwestern United States. However, each region has different drivers. Some prioritize utility-scale dispatchable power, while others focus on industrial heat, desalination, energy security, or green hydrogen. Through 2035, regional winners will be those that align policy, financing, industrial demand, and project execution capability.

Asia-Pacific, the Middle East and Africa, parts of Europe, Latin America, and North America will all offer opportunities, but growth will be strongest where solar resources, industrial demand, and supportive policy frameworks overlap.

Key Takeaway

The market will not grow evenly worldwide. It will cluster in high-solar-resource regions with strong clean energy and industrial heat demand.

Strategic Implication

Developers should prioritize regions where parabolic trough systems solve specific energy problems, not simply where sunlight is abundant.

North America offers opportunities in the southwestern United States and parts of Mexico. The United States has a history of CSP deployment and strong technical expertise, but competition from solar PV, batteries, and evolving renewable policy can influence project economics. The strongest opportunities may come from industrial heat, long-duration storage, and hybrid renewable projects rather than traditional CSP-only power plants. Mexico may offer potential where industrial growth, solar resources, and energy security needs converge.

Europe presents a mixed landscape. Northern Europe has limited solar thermal resource for parabolic trough deployment, but Southern Europe offers stronger potential, especially Spain, Italy, Greece, and parts of Portugal. Europe’s decarbonization policies, carbon pricing, and industrial emissions reduction goals could support solar thermal heat applications. However, land constraints, permitting, and competition from other renewables may limit large utility-scale deployment.

Asia-Pacific is one of the most important long-term regions. India has strong solar resources, growing electricity demand, industrial heat requirements, and policy interest in renewable energy. China has industrial manufacturing strength and has deployed various CSP technologies. Australia has excellent solar resources, mining demand, and remote energy needs. Southeast Asia may offer selective opportunities in industrial heat and agro-processing, although humidity and solar resource profiles vary.

Latin America has attractive potential in Chile, Peru, Mexico, Brazil, and Argentina. Chile is particularly relevant because of its strong solar resources, mining sector, and need for clean industrial energy. Mining operations can use solar thermal systems to reduce diesel and gas dependence. Brazil may offer industrial heat potential, while Argentina and Peru may develop selective projects linked to mining, desalination, or energy diversification.

The Middle East and Africa represent one of the most strategic regions. Countries in the Gulf, North Africa, and Southern Africa have strong direct solar irradiation, land availability, desalination needs, and energy diversification goals. Solar thermal systems can support electricity generation, water desalination, industrial heat, and green hydrogen strategies. Water scarcity remains a challenge, making dry cooling and low-water cleaning essential.

Regional risks include policy uncertainty, financing limitations, grid connection delays, currency volatility, local content requirements, water constraints, and competition from subsidized alternatives. Successful market entry requires local partnerships, accurate solar resource assessment, strong government engagement, and bankable project structures.

Why It Matters

Regional selection determines project viability more than global market averages.

Business Impact

Companies that localize solutions for regional energy needs will outperform generic technology suppliers.

Future Outlook

By 2035, growth will be concentrated in sun-rich regions with industrial heat demand, storage needs, and supportive policy frameworks.

Supply Chain, Manufacturing, and Trade Analysis

The supply chain for parabolic trough collectors combines global specialization with opportunities for regional localization. High-value components such as receiver tubes, selective coatings, precision mirrors, tracking drives, and thermal storage systems require specialized manufacturing expertise. At the same time, support structures, civil works, assembly, installation, piping, and maintenance can often be localized. Through 2035, supply chain resilience will become a decisive market factor as governments and developers seek lower logistics risk, domestic job creation, shorter project timelines, and stronger component availability.

The supply chain includes glass, steel, aluminum, receiver tubes, absorber coatings, tracking systems, thermal fluids, pumps, piping, control systems, storage tanks, EPC services, logistics providers, and maintenance firms.

Key Takeaway

Supply chain strength is essential because project reliability depends on component quality and long-term spare parts availability.

Strategic Implication

Manufacturers should develop regional partnerships while protecting quality standards for critical components.

Production begins with materials. Low-iron glass is used for mirrors because high reflectivity improves solar capture. Steel and aluminum support structures provide mechanical strength. Receiver tubes require specialized metals, coatings, and glass envelopes. Heat transfer systems require thermal fluids, pumps, valves, insulation, and piping designed for high temperatures.

Manufacturing involves both precision and scale. Mirrors must maintain accurate curvature and reflectivity. Receiver tubes must withstand thermal cycling, maintain vacuum insulation, and minimize heat loss. Tracking systems must operate reliably under dust, heat, wind, and mechanical stress. Storage tanks and heat exchangers must handle high temperatures and corrosion risks.

Raw material sourcing can be affected by energy prices, metal prices, glass capacity, specialty coating availability, and transportation costs. Large projects require significant volumes of materials, making procurement planning critical. Delays in one component category can disrupt project schedules.

Logistics infrastructure matters because parabolic trough projects involve large components, remote sites, and heavy construction activity. Mirrors and receiver tubes require careful handling to avoid damage. Transporting large structures to desert or remote industrial sites can be costly. Regional manufacturing or assembly hubs can reduce these risks.

Trade flows are influenced by renewable energy policies, tariffs, domestic content rules, and strategic industrial policy. Countries seeking clean energy manufacturing may support local production of structures, mirrors, and assembly systems. However, overly strict localization rules can increase project costs if local suppliers lack technical capability.

Supply chain resilience is becoming more important due to geopolitical uncertainty, shipping disruptions, currency movements, and critical material constraints. Developers increasingly prefer suppliers with diversified manufacturing footprints, inventory strategies, spare parts programs, and long-term service commitments.

By 2035, the supply chain is likely to become more regionalized. High-volume markets may develop local mirror production, steel structures, assembly plants, and service networks. Specialized receiver technologies may remain more concentrated, but partnerships and licensing could expand regional availability.

Why It Matters

Supply chain reliability affects project cost, construction timeline, plant availability, and investor confidence.

Business Impact

Suppliers with resilient, localized, and quality-controlled supply chains will gain a competitive advantage.

Future Outlook

By 2035, regional manufacturing ecosystems will become a major factor in project competitiveness.

Investment and Funding Landscape

Investment in the Parabolic Trough Collector Market is shifting from traditional utility-scale CSP financing toward broader clean energy infrastructure funding. Investors are evaluating the technology through the lens of dispatchable renewable power, thermal storage, industrial decarbonization, energy security, and long-duration flexibility. While capital intensity remains a challenge, parabolic trough systems can attract infrastructure capital when projects offer stable contracts, proven technology, predictable performance, and clear offtake arrangements. Through 2035, investment will increasingly flow into hybrid renewable projects, solar industrial heat platforms, thermal storage integration, desalination-energy systems, and clean energy hubs.

Capital is likely to flow into utility-scale CSP with storage, industrial heat systems, hybrid PV-CSP projects, thermal storage assets, receiver tube innovation, digital monitoring, and renewable heat service models.

Key Takeaway

Investment success depends on matching technology value with bankable revenue structures.

Strategic Implication

Developers should design projects around long-term contracts, storage value, industrial fuel displacement, and carbon reduction economics.

Capital expenditure trends in parabolic trough projects are shaped by solar field cost, thermal storage cost, power block cost, land preparation, grid connection, financing cost, and construction risk. Projects require higher upfront investment than many modular renewables, but they can deliver longer-duration value when storage and heat applications are included.

Venture investment may focus less on full-scale plant development and more on enabling technologies. These include advanced receiver tubes, selective coatings, high-temperature fluids, robotic cleaning, AI-based solar field monitoring, thermal storage materials, modular collector designs, and industrial heat control platforms.

Strategic investments may come from utilities, oil and gas companies, industrial firms, infrastructure funds, engineering companies, and sovereign wealth funds. Energy-intensive companies may invest in solar thermal systems to reduce fuel consumption, carbon exposure, and long-term energy price volatility.

Mergers and acquisitions may involve component specialists, EPC firms, storage technology companies, and digital monitoring providers. Larger energy infrastructure players may acquire niche technology providers to build integrated renewable heat capabilities.

Infrastructure spending will be important. Parabolic trough projects often require land development, grid connection, water systems, roads, storage tanks, and power blocks. Public-private partnerships may support projects in regions seeking energy diversification and industrial development.

Future investment outlook depends heavily on policy design. If clean energy incentives reward only electricity output, parabolic trough systems may face pressure from solar PV. If policies reward dispatchability, thermal storage, industrial heat decarbonization, and avoided fossil fuel use, investment attractiveness improves significantly.

By 2035, investors will likely classify parabolic trough opportunities into three categories. The first category will be utility-scale dispatchable renewable power projects. The second will be industrial heat and steam supply platforms. The third will be hybrid infrastructure projects combining solar PV, CSP, storage, desalination, hydrogen, or industrial energy services.

Why It Matters

Investment availability determines whether technology potential becomes commercial deployment.

Business Impact

Bankable contracts, proven performance, and clear revenue models will be essential for attracting capital.

Future Outlook

By 2035, the most attractive investments will combine storage, industrial heat demand, and long-term offtake agreements.

Regulatory, ESG, and Sustainability Factors

Regulatory, ESG, and sustainability factors are increasingly important to the Parabolic Trough Collector Market because the technology directly supports renewable energy, fossil fuel displacement, industrial decarbonization, and energy security. However, regulatory support must be designed carefully. Policies that focus only on low-cost electricity may favor solar PV, while policies that value clean heat, storage, dispatchability, and carbon reduction can strengthen parabolic trough adoption. ESG considerations also include land use, water consumption, local community impact, supply chain transparency, recycling, and lifecycle emissions. Through 2035, sustainability performance will become a core requirement for project approval and financing.

Regulatory drivers include renewable energy targets, carbon reduction policies, clean heat incentives, storage support, industrial decarbonization programs, permitting rules, environmental regulations, and ESG financing requirements.

Key Takeaway

Parabolic trough systems benefit most from policies that recognize clean thermal energy and dispatchable renewable power.

Strategic Implication

Stakeholders should engage policymakers to ensure solar thermal heat, storage, and industrial decarbonization are properly valued.

Government policies shape market demand through renewable portfolio standards, clean energy auctions, tax incentives, carbon pricing, industrial decarbonization funds, green public procurement, and energy security strategies. In some regions, CSP has struggled when procurement focused only on lowest-cost electricity. Future policy frameworks need to recognize grid flexibility, thermal storage, and clean heat value.

Regulatory compliance includes land permits, environmental impact assessments, grid connection rules, water use permissions, construction approvals, safety regulations, and industrial integration standards. Large projects require careful planning to manage biodiversity, land rights, cultural heritage, and local community concerns.

Environmental impact is generally favorable compared with fossil fuel-based heat and power, but projects must manage land footprint, mirror glare, habitat disturbance, water use, and end-of-life recycling. Dry cooling and robotic cleaning can reduce water use, while careful site selection can reduce ecological impact.

Sustainability initiatives include local employment, domestic manufacturing, low-carbon materials, recycling of glass and metals, responsible sourcing, digital efficiency optimization, and integration with carbon reduction strategies. These initiatives can improve project acceptance and financing access.

ESG considerations are increasingly linked to capital allocation. Institutional investors often prefer assets that demonstrate measurable emissions reduction, transparent governance, strong safety standards, and community benefit. Parabolic trough projects can align well with ESG requirements if they document lifecycle emissions, water strategy, supply chain standards, and local economic contribution.

Future policy direction is likely to place greater emphasis on industrial heat decarbonization and long-duration storage. This could create a stronger regulatory environment for parabolic trough collectors than electricity-only incentives.

Why It Matters

Policy design can either unlock or limit the market’s potential.

Business Impact

Projects with strong ESG credentials and regulatory alignment will have better access to capital.

Future Outlook

By 2035, clean heat and storage policy will become central to market expansion.

Future Opportunities and Emerging Business Models

Future opportunities in the Parabolic Trough Collector Market will increasingly emerge outside traditional utility-scale CSP power generation. The next growth phase will be driven by industrial solar heat, heat-as-a-service, hybrid renewable energy hubs, solar desalination, green hydrogen support systems, thermal storage retrofits, and digital asset optimization. Business models will also evolve from equipment sales to energy services, long-term heat contracts, performance-based O&M, and integrated infrastructure ownership. Through 2035, the strongest opportunities will come from solving customer-specific energy problems rather than selling collector hardware alone.

Emerging opportunities include industrial heat supply, hybrid PV-CSP plants, thermal storage services, solar desalination, mining energy systems, green hydrogen hubs, district heating, digital monitoring, robotic cleaning, and heat purchase agreements.

Key Takeaway

Future growth will be driven by business model innovation as much as technology innovation.

Strategic Implication

Companies should develop recurring revenue models based on heat delivery, performance, storage, and lifecycle services.

New revenue streams include long-term solar heat supply contracts, energy-as-a-service models, thermal storage leasing, digital performance subscriptions, receiver replacement services, robotic cleaning services, and hybrid plant optimization software. These models reduce customer upfront cost and create recurring revenue for providers.

Untapped markets include industrial clusters in high-solar regions, remote mining operations, desalination facilities, agro-processing zones, district heating networks, and industrial parks. Many of these customers need reliable heat and may be willing to adopt solar thermal systems if financing and integration risks are managed.

Digital business models are becoming more attractive. Solar field monitoring platforms can track mirror reflectivity, receiver performance, thermal losses, cleaning needs, and equipment health. Predictive analytics can reduce downtime and improve output. For asset owners, software can improve revenue by optimizing when to store heat, generate power, or supply industrial processes.

Technology disruptions may include high-temperature molten salt troughs, advanced coatings, low-cost modular collectors, autonomous cleaning robots, AI-based energy management, and integrated thermal batteries. These innovations could improve competitiveness and open new applications.

Long-term opportunities are strongest where parabolic trough systems become part of broader clean infrastructure. For example, a desert industrial hub may combine solar PV, parabolic trough collectors, thermal storage, batteries, desalination, hydrogen production, and industrial steam networks. In such systems, parabolic trough collectors provide valuable thermal energy and storage flexibility.

Heat-as-a-service may become one of the most important business models. Under this model, a developer finances, owns, and operates the solar thermal system while the customer pays for delivered heat. This reduces capital burden for industrial users and creates stable long-term revenue for developers.

Why It Matters

Business model innovation can reduce adoption barriers and expand the market beyond traditional CSP buyers.

Business Impact

Recurring service and heat revenue can improve margins and customer retention.

Future Outlook

By 2035, many parabolic trough projects will be structured as integrated energy service platforms.

Strategic Outlook Through 2035

Through 2035, the Parabolic Trough Collector Market is expected to transform from a CSP equipment market into a broader solar thermal infrastructure market. The technology’s future will depend on its ability to deliver dispatchable renewable power, industrial heat, storage flexibility, and fossil fuel displacement in applications where solar PV alone is insufficient. The market will not grow uniformly across all regions or end uses. Growth will concentrate in high-solar-resource markets with supportive policy, industrial heat demand, energy security needs, and financing capability. Strategic winners will be companies that combine efficient hardware, thermal storage, digital operations, local execution, and bankable business models.

By 2035, parabolic trough collectors are likely to be used in utility-scale renewable power plants, industrial heat systems, hybrid solar infrastructure, desalination facilities, mining operations, district heating networks, and clean energy hubs.

Key Takeaway

The market’s long-term future depends on positioning parabolic trough collectors as flexible clean heat and storage infrastructure.

Strategic Implication

Stakeholders should prioritize integrated solutions, industrial applications, thermal storage, and regional execution capability.

The industry transformation scenario through 2035 will be shaped by three forces. First, electricity systems will need more flexibility as solar PV and wind penetration rises. Second, industries will need practical ways to decarbonize heat. Third, governments will seek energy security and domestic renewable resources. Parabolic trough collectors can contribute to all three priorities if deployed strategically.

Future market evolution will likely favor hybridization. Standalone CSP plants may still be built in selected regions, but hybrid PV-CSP-storage systems will become more attractive. In these systems, PV provides low-cost electricity, while parabolic trough collectors provide heat and storage. This allows better use of land, transmission infrastructure, and energy management systems.

Strategic recommendations for manufacturers include investing in higher-efficiency receivers, durable mirrors, modular structures, low-water cleaning technologies, and digital monitoring. Developers should focus on bankable offtake contracts, industrial heat customers, local partnerships, and integrated project designs. Policymakers should create incentives that value dispatchability, renewable heat, carbon reduction, and storage duration.

Key success factors will include cost reduction, project execution discipline, component reliability, financing access, regulatory alignment, storage integration, and customer education. The market will reward companies that can simplify adoption for utilities and industrial users.

Executive conclusions are clear. Parabolic trough collectors are not likely to replace solar PV as the dominant renewable electricity technology. However, they do not need to. Their value lies in heat, storage, reliability, and industrial decarbonization. When these values are monetized, the technology can remain highly relevant through 2035.

Long-term outlook through 2035 is positive but selective. Growth will depend on regional energy strategies, policy design, and the ability of suppliers to reduce cost while improving reliability. The most attractive opportunities will be in the Middle East, North Africa, India, Australia, Chile, Southern Europe, and selected North American markets.

Why It Matters

The market sits at the intersection of renewable energy, storage, industrial heat, and decarbonization.

Business Impact

Companies that adapt to integrated energy infrastructure will outperform those that remain focused only on collector hardware.

Future Outlook

By 2035, parabolic trough collectors will remain a specialized but strategically important clean energy technology.

Top 10 Industry Trends

1. Shift Toward Dispatchable Renewable Power

The market is increasingly shaped by demand for renewable power that can be delivered when needed. Solar PV and wind are expanding quickly, but their variability creates grid balancing challenges. Parabolic trough collectors, when paired with thermal energy storage, can generate electricity beyond daylight hours. This gives the technology strategic relevance in power systems with high renewable penetration. Through 2035, dispatchability will become a key differentiator because utilities will value reliability, flexibility, and evening peak supply.

2. Growth of Thermal Energy Storage Integration

Thermal energy storage is becoming central to parabolic trough project economics. Storage allows captured solar heat to be used after sunset or during periods of high demand. Molten salt systems, advanced thermal media, and improved storage tanks can increase project value. Through 2035, storage-enabled projects will be more competitive than systems that only generate daytime electricity.

3. Expansion into Industrial Process Heat

Industrial heat is one of the largest long-term opportunities. Many industries require steam and medium-temperature heat, which parabolic trough collectors can provide. Food processing, chemicals, textiles, mining, desalination, and refining are attractive use cases. Through 2035, industrial decarbonization will push more companies to evaluate solar thermal heat.

4. Hybrid PV-CSP Project Development

Hybrid renewable projects are gaining importance. Solar PV can generate low-cost electricity during the day, while parabolic trough systems can provide heat storage and evening power. This combination improves renewable reliability and reduces curtailment. Through 2035, hybrid project design will become a major trend in high-solar regions.

5. Digital Solar Field Optimization

Digital monitoring, artificial intelligence, sensors, drones, and predictive maintenance are transforming solar field operations. These tools help identify mirror soiling, receiver degradation, tracking errors, and fluid system inefficiencies. Through 2035, digital performance platforms will become standard for large projects.

6. Water-Efficient Operations

Water scarcity is a major issue in many high-solar regions. Future projects will increasingly use dry cooling, robotic cleaning, dust-resistant mirrors, and low-water maintenance systems. Through 2035, water efficiency will become a key permitting and ESG requirement.

7. Localization of Manufacturing

Governments and developers are seeking local manufacturing to reduce import dependence and create jobs. Steel structures, assembly, installation, and maintenance can be localized in many regions. Through 2035, regional manufacturing hubs will become more important for project competitiveness.

8. Advanced Receiver Tube Innovation

Receiver tubes are critical to efficiency. Improvements in absorber coatings, vacuum stability, corrosion resistance, and high-temperature performance can increase energy output. Through 2035, receiver innovation will remain a key technology battleground.

9. Emergence of Heat-as-a-Service

Industrial customers may prefer paying for delivered heat rather than owning solar thermal assets. Heat-as-a-service models reduce upfront investment and transfer operational responsibility to specialized providers. Through 2035, this model could accelerate adoption among industrial users.

10. Integration with Clean Energy Hubs

Parabolic trough collectors may become part of larger energy hubs that include solar PV, batteries, thermal storage, desalination, hydrogen, and industrial steam networks. Through 2035, integrated energy hubs will create new opportunities for solar thermal infrastructure.

Top 10 Growth Opportunities

1. Utility-Scale CSP with Storage

Utility-scale projects with thermal storage remain an important opportunity in regions with strong solar resources and evening peak demand. These projects can provide renewable electricity after sunset and support grid stability. Through 2035, they will be most attractive where policy rewards dispatchability.

2. Industrial Steam Supply

Industrial steam is a major growth opportunity because many factories still depend on fossil fuel boilers. Parabolic trough systems can reduce fuel use and emissions. Food processing, chemicals, textiles, and pharmaceuticals are attractive sectors.

3. Solar Desalination

Water-stressed regions can use solar thermal systems to support desalination. This opportunity is particularly relevant in the Middle East, North Africa, and parts of Asia-Pacific. Through 2035, water-energy integration will become more strategic.

4. Mining Energy Systems

Remote mining operations often face high diesel costs and energy security issues. Parabolic trough collectors can provide heat and support hybrid power systems. This is attractive in Chile, Australia, Africa, and parts of Latin America.

5. Hybrid PV-CSP Plants

Hybrid projects can combine low-cost PV with thermal storage and dispatchable output. This improves energy reliability and asset utilization. Through 2035, hybrid plants will become more common in solar-rich regions.

6. District Heating Networks

Cities seeking low-carbon heating can integrate solar thermal systems into district heating networks. Parabolic trough collectors can support large-scale heat generation when land and solar resources are available.

7. Thermal Storage Retrofits

Existing CSP and industrial heat systems may need improved storage. Retrofitting storage systems can enhance performance and revenue. This creates opportunities for storage technology providers and EPC firms.

8. Green Hydrogen Support Infrastructure

Parabolic trough collectors can support hydrogen hubs through thermal energy, water treatment, and hybrid renewable integration. Future high-temperature applications may strengthen this opportunity.

9. Food and Beverage Processing

Food processing uses significant thermal energy for drying, washing, sterilization, and cooking. Solar thermal heat can reduce fossil fuel dependence and improve sustainability credentials.

10. Digital O&M Services

Digital monitoring, predictive maintenance, and performance analytics can create recurring service revenue. As installed capacity grows, O&M platforms will become increasingly valuable.

Top 10 Investment Opportunities

1. Advanced Receiver Tubes

Receiver tubes directly influence system efficiency and reliability. Investment in coatings, materials, vacuum performance, and high-temperature durability can generate strong technology value.

2. Molten Salt Storage Systems

Thermal storage is central to dispatchability. Investment in molten salt systems, storage tanks, heat exchangers, and corrosion management will remain attractive through 2035.

3. Industrial Solar Heat Platforms

Companies that finance, own, and operate solar heat systems for industrial customers can build recurring revenue through long-term heat contracts.

4. Robotic Cleaning Technologies

Dust and soiling reduce mirror efficiency. Robotic cleaning technologies can reduce water use and improve plant output, especially in desert markets.

5. Digital Twin Platforms

Digital twins can improve performance forecasting, maintenance planning, and asset optimization. This is attractive for large solar thermal plants and industrial heat systems.

6. Hybrid Renewable Project Development

Investment in projects combining PV, CSP, batteries, and thermal storage can improve grid value and reduce revenue risk.

7. Local Manufacturing Hubs

Regional manufacturing for mirrors, structures, and assembly can reduce logistics cost and support domestic content policies.

8. Solar Desalination Infrastructure

Water scarcity creates demand for clean desalination energy. Solar thermal desalination projects can attract infrastructure and sovereign investment.

9. High-Temperature Fluids

Investment in advanced heat transfer fluids can improve system efficiency and expand industrial applications.

10. Performance-Based O&M Companies

Specialized O&M companies can generate recurring revenue by improving plant availability, cleaning efficiency, and thermal performance.

Top 10 Risks

1. Competition from Solar PV and Batteries

Solar PV and batteries are improving rapidly and may limit CSP growth in electricity-only applications. Parabolic trough projects must prove value through storage, heat, and dispatchability.

2. High Capital Cost

Large upfront investment can reduce project attractiveness. Financing structures, policy support, and cost reduction are essential.

3. Project Execution Delays

CSP projects are complex and can face delays in permitting, construction, grid connection, and commissioning.

4. Receiver Tube Degradation

Receiver performance affects efficiency. Vacuum loss, coating degradation, and thermal stress can reduce output.

5. Mirror Soiling and Cleaning Cost

Dust, sand, and pollution reduce reflectivity. Cleaning costs and water availability are major operational risks.

6. Heat Transfer Fluid Limitations

Traditional thermal oils have temperature limits and safety requirements. Fluid degradation can increase maintenance cost.

7. Water Availability

Many high-solar regions are water-stressed. Cooling and cleaning strategies must be carefully managed.

8. Policy Uncertainty

Changes in renewable incentives, tariffs, tax credits, or procurement rules can affect project economics.

9. Supply Chain Dependence

Specialized components may depend on limited suppliers. Logistics delays and import restrictions can increase risk.

10. Customer Adoption Barriers

Industrial users may hesitate due to unfamiliarity, integration concerns, and capital constraints. Education and service-based models are needed.

Executive Questions and Answers

1. What is the Parabolic Trough Collector Market?

The market includes technologies, components, projects, and services related to solar thermal systems that use curved mirrors to concentrate sunlight onto receiver tubes. These systems convert direct solar radiation into heat for electricity generation, industrial processes, thermal storage, desalination, and hybrid renewable systems. Its strategic importance lies in the ability to provide renewable thermal energy that can be stored and dispatched.

2. What is driving market growth?

Growth is driven by renewable energy targets, industrial decarbonization, energy security, grid flexibility, and demand for long-duration thermal storage. The market benefits where users need heat, not only electricity.

3. Why is thermal storage important?

Thermal storage allows solar heat to be used after sunset or during peak demand. This makes parabolic trough systems more flexible than solar-only generation and improves their value in power and industrial applications.

4. Which regions will lead growth?

High-solar-resource regions such as the Middle East, North Africa, India, Australia, Chile, Southern Europe, and the southwestern United States are likely to lead selected deployment.

5. What are the main end-user industries?

Utilities, industrial manufacturers, mining companies, desalination facilities, food processors, chemical producers, refineries, district heating operators, and hydrogen developers are key end users.

6. How does the technology compare with solar PV?

Solar PV is usually cheaper for daytime electricity. Parabolic trough collectors are more valuable where heat, storage, dispatchability, and industrial steam are required.

7. What are the biggest risks?

Major risks include high capital cost, competition from PV and batteries, water constraints, component degradation, policy uncertainty, and project execution complexity.

8. What technologies are reshaping the market?