-

Écrivez-nous

- Rapports phares

Railway Propulsion Systems Market

Publié le 23 June, 2026

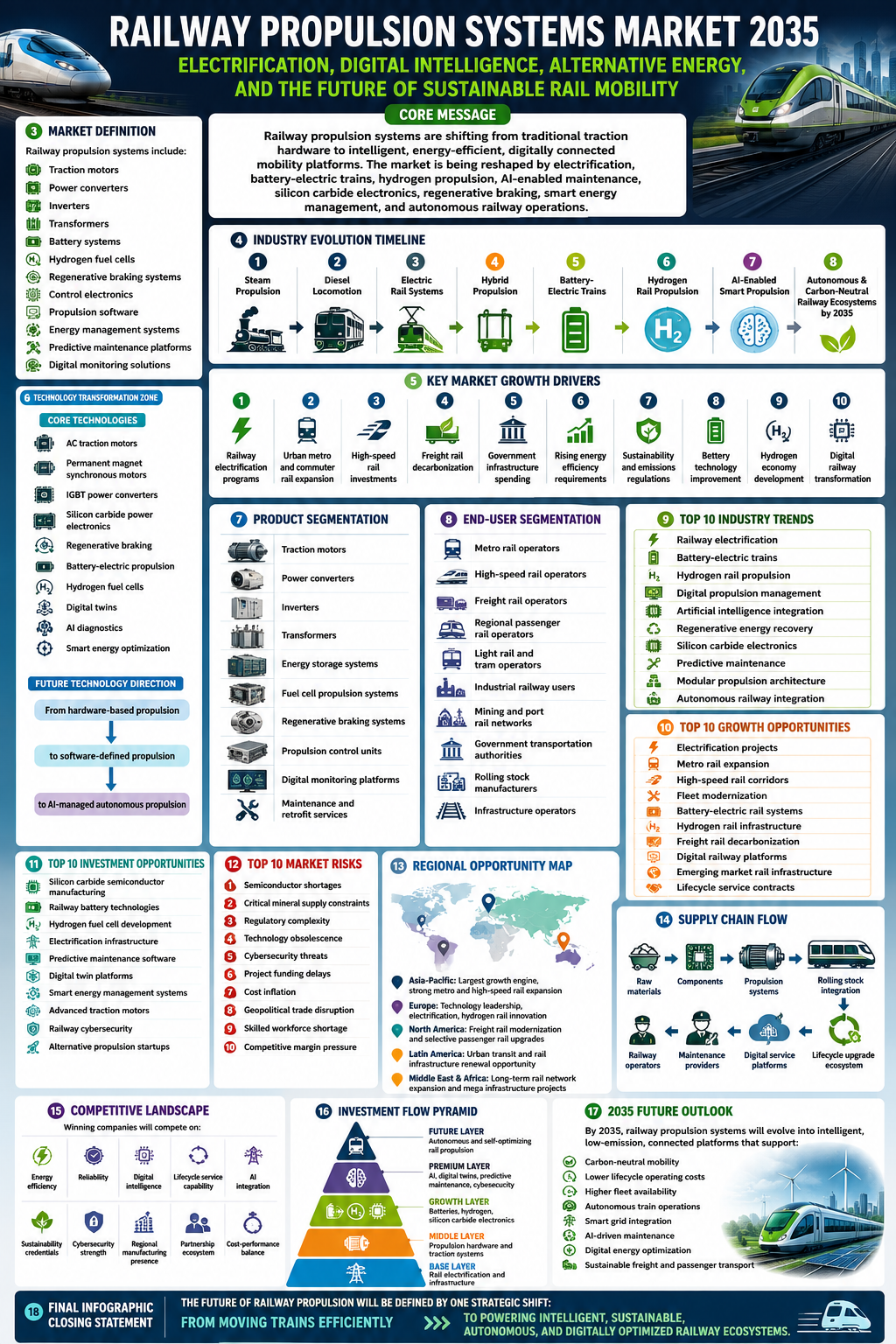

The Railway Propulsion Systems Market represents one of the most strategically important segments within the global rail transportation industry. Railway propulsion systems comprise the complete set of technologies, components, software, and power conversion equipment responsible for generating, controlling, and transmitting power required for train movement. These systems typically include traction motors, power converters, inverters, transformers, control electronics, energy management systems, onboard software platforms, and associated auxiliary equipment. Whether deployed in high-speed passenger trains, metro rail networks, commuter trains, freight locomotives, or light rail transit systems, propulsion technology serves as the operational backbone that determines efficiency, reliability, speed, safety, and lifecycle economics.

Historically, railway propulsion has evolved alongside broader industrial and transportation revolutions. Early railways relied heavily on steam-based propulsion, which dominated global rail transportation for more than a century. The transition toward diesel locomotives accelerated during the twentieth century as rail operators sought greater operational flexibility and reduced infrastructure dependence. However, growing urbanization, environmental concerns, energy efficiency requirements, and technological innovation eventually shifted industry focus toward electric propulsion systems. Electrification transformed rail transport economics by improving energy utilization, reducing operating costs, enhancing acceleration performance, and enabling higher passenger capacities.

The modern railway propulsion systems market is increasingly characterized by digitalization, electrification, automation, and sustainability objectives. Governments worldwide are investing heavily in railway modernization initiatives as transportation networks become central to economic growth, carbon reduction strategies, and urban mobility planning. Rail transport is widely recognized as one of the most energy-efficient modes of mass transportation, creating favorable conditions for propulsion technology investments. Consequently, operators are prioritizing advanced propulsion solutions capable of delivering higher efficiency, lower emissions, predictive maintenance capabilities, and improved passenger experiences.

The strategic significance of propulsion systems extends beyond train movement alone. Propulsion technology directly influences infrastructure utilization, maintenance requirements, operating costs, fleet availability, environmental performance, and long-term asset value. For railway operators managing large fleets, even marginal improvements in propulsion efficiency can generate substantial cost savings over decades of operation. As a result, procurement decisions increasingly focus on total lifecycle value rather than initial acquisition cost.

Now Get Free PDF Report on : Global Railway Propulsion Systems Market Strategic Recommendations 2026-2033 : https://www.statsndata.org/download-sample.php?id=148207

Current industry dynamics indicate a strong shift toward intelligent propulsion architectures. Advanced semiconductor technologies, digital control systems, regenerative braking solutions, energy storage integration, and real-time monitoring capabilities are reshaping industry standards. The emergence of battery-electric trains, hydrogen-powered rail vehicles, hybrid propulsion platforms, and next-generation traction systems is further expanding technological possibilities. Simultaneously, rising demand for urban transit systems, high-speed rail corridors, and sustainable freight transportation is creating new opportunities for propulsion manufacturers and technology suppliers.

Looking toward 2035, railway propulsion systems will become increasingly integrated with broader transportation digitization ecosystems. Artificial intelligence, predictive analytics, autonomous train operations, and smart energy management platforms are expected to redefine propulsion system performance standards. Consequently, the market is transitioning from a component-focused industry toward a software-enabled mobility technology sector where efficiency, connectivity, sustainability, and intelligence become equally important competitive differentiators.

2. Market Ecosystem and Value Chain Analysis

The railway propulsion systems market operates within a highly specialized and interconnected ecosystem involving raw material suppliers, component manufacturers, system integrators, rolling stock producers, infrastructure operators, maintenance providers, and transportation authorities. Each participant contributes value at different stages of the supply chain, collectively determining product performance, reliability, and commercial success.

At the foundation of the ecosystem lies the raw material supply network. Railway propulsion systems require substantial quantities of copper, aluminum, electrical steel, silicon, rare earth materials, advanced polymers, composite materials, and semiconductor-grade silicon. Copper remains particularly important because of its extensive use in traction motors, transformers, power distribution systems, and electrical wiring. Electrical steel plays a critical role in minimizing energy losses within motors and transformers, while rare earth elements support the production of high-performance permanent magnet motors increasingly adopted across modern rail applications.

Component manufacturers occupy the next stage of the value chain. These companies specialize in producing traction motors, insulated-gate bipolar transistor (IGBT) modules, silicon carbide power devices, converters, inverters, transformers, cooling systems, braking systems, sensors, controllers, and software platforms. Increasing technological sophistication has elevated the importance of electronics suppliers as propulsion systems become more digitally controlled and software dependent.

System integration represents one of the most critical value-creation stages. Railway propulsion systems must seamlessly integrate mechanical, electrical, electronic, and software components while meeting stringent safety and reliability standards. System integrators combine diverse technologies into fully functional propulsion architectures optimized for specific train types, operating environments, and customer requirements. Successful integration directly impacts energy efficiency, operational reliability, and maintenance performance.

Rolling stock manufacturers serve as major downstream customers for propulsion providers. These manufacturers incorporate propulsion systems into passenger trains, metro vehicles, freight locomotives, light rail vehicles, and high-speed rail platforms. Collaboration between rolling stock manufacturers and propulsion suppliers often begins during early design phases to ensure compatibility between propulsion technologies and overall vehicle architecture.

Railway operators constitute the ultimate end users within the ecosystem. Their purchasing decisions are increasingly influenced by lifecycle costs, energy efficiency, maintenance requirements, digital capabilities, and sustainability objectives. Operators seek propulsion systems that maximize fleet availability while minimizing operating expenditures and environmental impact.

Aftermarket service providers have become increasingly important contributors to value creation. Modern propulsion systems generate substantial operational data that can be leveraged for predictive maintenance, performance optimization, and asset management. Service providers increasingly offer long-term maintenance contracts, digital monitoring services, remote diagnostics, and performance improvement programs.

Value creation within the railway propulsion ecosystem is shifting from hardware-centric manufacturing toward integrated lifecycle solutions. Revenue streams increasingly extend beyond equipment sales to include software subscriptions, maintenance agreements, analytics services, digital upgrades, and energy optimization solutions. This transition reflects broader industry trends emphasizing long-term customer relationships, recurring revenue generation, and continuous operational improvement.

As railway networks continue expanding globally, ecosystem participants capable of delivering integrated, data-driven, and sustainability-focused solutions are likely to capture greater market share. The value chain is expected to become increasingly collaborative, digitally connected, and innovation driven through 2035.

Technology Landscape and Industry Innovation

Technology development remains the primary force transforming the railway propulsion systems market. Advances in power electronics, semiconductor materials, digital controls, energy storage technologies, and intelligent software systems are fundamentally changing how trains generate, manage, and utilize energy.

At the core of modern propulsion systems are traction motors, which convert electrical energy into mechanical motion. Traditional DC motors have largely been replaced by advanced AC induction motors and permanent magnet synchronous motors. These technologies offer superior efficiency, reduced maintenance requirements, improved reliability, and enhanced power density. Permanent magnet technologies, in particular, are attracting growing attention because of their ability to deliver higher efficiency levels while reducing overall system size and weight.

Power electronics represent another critical area of innovation. Historically, insulated-gate bipolar transistor technologies dominated railway propulsion applications. However, the emergence of silicon carbide semiconductors is creating a major technological shift. Silicon carbide devices enable higher switching frequencies, reduced energy losses, improved thermal performance, smaller cooling requirements, and increased system efficiency. These benefits translate directly into lower operating costs and improved train performance.

Digital control technologies are becoming increasingly sophisticated. Modern propulsion systems incorporate advanced control algorithms capable of continuously optimizing power consumption, traction performance, braking efficiency, and system reliability. Real-time monitoring capabilities allow operators to detect anomalies before failures occur, significantly reducing maintenance costs and service disruptions.

Artificial intelligence and machine learning are emerging as transformative technologies within railway propulsion. AI-powered predictive maintenance systems analyze operational data to identify component degradation patterns, forecast maintenance needs, and optimize maintenance schedules. These capabilities improve fleet availability while reducing unplanned downtime.

Energy recovery technologies are also advancing rapidly. Regenerative braking systems allow trains to recover kinetic energy during deceleration and either return it to the grid or store it for future use. This capability significantly improves overall energy efficiency and supports sustainability objectives. As energy prices rise globally, regenerative technologies are becoming increasingly valuable economic assets.

Battery-electric propulsion systems are gaining momentum, particularly for regional rail routes where full electrification may be economically challenging. Improvements in battery energy density, charging infrastructure, and battery management systems are expanding operational feasibility. Similarly, hydrogen fuel cell propulsion technologies are emerging as viable alternatives for non-electrified rail corridors seeking zero-emission operations.

The technology roadmap toward 2035 suggests increasing convergence between propulsion systems and broader digital transportation ecosystems. Autonomous train operations, intelligent traffic management systems, cloud-based analytics platforms, digital twins, and integrated energy management solutions are expected to become standard features. Future propulsion systems will not simply provide movement but will function as intelligent, interconnected assets capable of optimizing performance across entire rail networks.

This technological evolution is expected to redefine competitive dynamics throughout the industry. Companies investing aggressively in advanced electronics, digital capabilities, energy efficiency technologies, and software integration are likely to establish significant long-term advantages as railway operators prioritize operational intelligence alongside traditional performance metrics.

Major Growth Drivers

The Railway Propulsion Systems Market is benefiting from multiple structural growth drivers that extend well beyond traditional railway expansion. These drivers are rooted in global economic development, urbanization, sustainability objectives, transportation modernization, and technological progress.

One of the strongest growth catalysts is rapid urbanization. Major metropolitan regions worldwide continue experiencing population growth that places increasing pressure on transportation infrastructure. Governments and city planners are responding by expanding metro systems, suburban rail networks, light rail transit systems, and high-capacity passenger transportation corridors. Each new rail project requires advanced propulsion technologies capable of supporting reliable, efficient, and high-frequency operations.

Environmental sustainability objectives represent another major growth driver. Transportation accounts for a significant share of global carbon emissions, prompting governments to prioritize low-emission mobility solutions. Rail transport offers substantial environmental advantages compared with road and air transportation. Consequently, national decarbonization strategies frequently include investments in railway expansion and modernization. These investments directly stimulate demand for advanced electric propulsion systems, regenerative braking technologies, and alternative energy propulsion platforms.

Infrastructure investment programs are also creating substantial market opportunities. Many countries are implementing long-term transportation infrastructure strategies designed to improve economic competitiveness, reduce congestion, and enhance connectivity. High-speed rail projects, cross-border transportation corridors, freight modernization initiatives, and urban transit expansions all contribute to rising propulsion system demand.

Freight transportation requirements are evolving as global supply chains become increasingly complex. Rail freight is gaining importance because of its cost efficiency, energy efficiency, and environmental advantages. Modern freight operators require propulsion systems capable of handling heavier loads, longer distances, and more demanding operating conditions. This trend is encouraging investments in higher-performance traction technologies and advanced locomotive propulsion systems.

Technology advancement itself functions as a growth driver by accelerating replacement cycles. Many existing rail fleets utilize aging propulsion technologies that are less efficient, more expensive to maintain, and incompatible with modern digital infrastructure. Operators are increasingly replacing outdated systems with advanced propulsion platforms that offer lower lifecycle costs and improved operational capabilities.

Government incentives further strengthen market expansion. Public funding programs, transportation grants, railway electrification initiatives, and sustainability-focused investment frameworks are reducing barriers to adoption. These policies are particularly important in emerging economies where transportation infrastructure development remains a national priority.

Digital transformation initiatives are creating additional demand. Railway operators increasingly seek propulsion systems capable of supporting predictive maintenance, real-time monitoring, fleet optimization, and operational analytics. As a result, software-enabled propulsion platforms are becoming essential components of broader railway modernization programs.

Looking ahead to 2035, the combined influence of urban mobility expansion, climate policy implementation, infrastructure investment, freight transportation growth, and technological innovation is expected to sustain robust demand for railway propulsion systems. These drivers are largely structural rather than cyclical, providing a strong foundation for long-term industry growth.

Market Challenges and Risk Factors

Despite strong long-term growth prospects, the Railway Propulsion Systems Market faces several significant challenges and risk factors that could influence investment decisions, technology adoption rates, and overall industry development.

One of the most prominent challenges involves supply chain complexity. Modern propulsion systems depend on highly specialized materials, advanced semiconductors, rare earth elements, and precision-engineered components sourced from global supply networks. Disruptions affecting semiconductor manufacturing, critical mineral availability, geopolitical trade relationships, or logistics infrastructure can create significant production bottlenecks. As propulsion systems become increasingly electronics-intensive, supply chain resilience is emerging as a critical competitive factor.

Cost pressures represent another major challenge. Railway propulsion systems require substantial research and development investments, rigorous testing procedures, certification processes, and long product development cycles. These factors contribute to high capital requirements and elevated production costs. Simultaneously, railway operators face budget constraints and increasing pressure to demonstrate economic value, creating ongoing tension between innovation and affordability.

Regulatory compliance adds additional complexity. Railway propulsion technologies must meet stringent safety, reliability, environmental, electromagnetic compatibility, and operational standards. Regulatory requirements vary across regions, increasing compliance costs for manufacturers seeking global market access. The certification process can be lengthy and resource intensive, potentially delaying commercialization timelines.

Technology adoption barriers also remain significant. Railway operators often manage assets with operational lifespans exceeding thirty years. Consequently, introducing new propulsion technologies requires extensive validation, risk assessment, and compatibility testing. Operators may hesitate to adopt emerging technologies if long-term reliability has not been fully demonstrated under real-world operating conditions.

Cybersecurity risks are becoming increasingly relevant as propulsion systems become more digitally connected. Integration with network management platforms, cloud-based analytics systems, and remote monitoring solutions expands potential vulnerability surfaces. A successful cyberattack affecting propulsion control systems could disrupt operations, compromise safety, and generate substantial financial losses.

Competitive pressures are intensifying as established industry participants compete alongside new technology-focused entrants. Differentiation is becoming more challenging because many core propulsion technologies are approaching maturity. Companies must increasingly compete through software capabilities, service offerings, digital integration, and lifecycle support rather than hardware performance alone.

Macroeconomic uncertainty represents another important risk factor. Railway infrastructure projects often depend on public funding and long-term government commitments. Economic downturns, fiscal constraints, changing political priorities, or budget reallocations can delay or reduce planned railway investments, affecting propulsion system demand.

Finally, technological disruption itself presents a dual challenge. While innovation creates opportunities, it can also render existing products obsolete more rapidly than anticipated. Manufacturers must carefully balance investment in current technologies against emerging solutions such as hydrogen propulsion, battery-electric systems, autonomous operations, and next-generation semiconductor platforms.

Through 2035, organizations capable of managing supply chain resilience, maintaining technological flexibility, ensuring regulatory compliance, and adapting to evolving customer expectations will be best positioned to navigate these risks while capturing long-term market opportunities.

6. Industry Trends Reshaping the Market

The Railway Propulsion Systems Market is undergoing a profound transformation as technological innovation, sustainability imperatives, and evolving transportation requirements reshape industry priorities. The trends emerging today are not merely incremental improvements but represent structural changes that will influence procurement strategies, technology investments, competitive positioning, and operational models through 2035.

One of the most significant trends is the accelerating shift toward complete railway electrification. Governments and railway operators are increasingly prioritizing electric propulsion systems due to their superior energy efficiency, lower operating costs, reduced emissions, and compatibility with long-term decarbonization strategies. Electrification is no longer limited to high-speed rail or metropolitan transit systems. Regional railways, freight corridors, and intercity routes are also becoming targets for electrification initiatives. This transition is driving substantial demand for advanced traction systems, intelligent converters, and energy-efficient propulsion platforms.

Another major trend involves the emergence of alternative propulsion technologies. Battery-electric trains, hydrogen fuel cell-powered trains, and hybrid propulsion systems are gaining momentum, particularly in regions where complete electrification remains economically challenging. These technologies are addressing the operational limitations associated with diesel-powered locomotives while enabling railway operators to meet increasingly stringent environmental regulations. As energy storage technologies mature and hydrogen infrastructure expands, alternative propulsion systems are expected to capture a growing share of future fleet investments.

Digitalization is reshaping propulsion system design and operation. Modern propulsion architectures increasingly incorporate sensors, connectivity platforms, cloud integration, and real-time analytics capabilities. The objective is no longer limited to moving trains efficiently. Operators now seek propulsion systems capable of continuously monitoring performance, predicting maintenance needs, optimizing energy consumption, and improving fleet availability. This trend is transforming propulsion systems from standalone mechanical assets into intelligent digital infrastructure components.

Artificial intelligence and machine learning are becoming central to operational optimization. Advanced algorithms analyze vast amounts of operational data to identify performance anomalies, forecast component failures, optimize maintenance schedules, and improve energy efficiency. The integration of AI into propulsion management systems enables operators to transition from reactive maintenance approaches toward predictive and condition-based maintenance strategies that significantly reduce lifecycle costs.

Energy efficiency has emerged as a major competitive differentiator. Rising electricity costs, sustainability commitments, and operating margin pressures are encouraging railway operators to prioritize propulsion systems capable of minimizing energy consumption. Regenerative braking technologies, lightweight propulsion components, advanced motor designs, and intelligent power management systems are becoming increasingly important investment priorities.

The industry is also witnessing a shift toward modular propulsion architectures. Traditional propulsion systems were often designed for specific train models, limiting flexibility and increasing lifecycle costs. Modern modular platforms allow operators and manufacturers to standardize components across multiple train types, simplifying maintenance, reducing inventory requirements, and improving scalability. This approach enhances operational flexibility while supporting faster deployment of new rolling stock programs.

Cybersecurity is emerging as a critical industry trend. As propulsion systems become more connected and digitally integrated, protecting operational technology networks from cyber threats is becoming a strategic necessity. Future propulsion platforms will increasingly incorporate cybersecurity-by-design principles to safeguard operational continuity and passenger safety.

Looking toward 2035, the convergence of electrification, alternative energy technologies, digital intelligence, energy optimization, and cybersecurity will redefine propulsion system requirements. Companies capable of aligning product development strategies with these long-term trends will be positioned to capture substantial market opportunities as the industry transitions toward more intelligent, sustainable, and connected railway ecosystems.

Product and Service Segment Analysis

The Railway Propulsion Systems Market encompasses a diverse range of products and services that collectively support train movement, power management, energy efficiency, operational reliability, and lifecycle performance. Understanding the relative importance and growth potential of each segment is essential for assessing future market dynamics and investment opportunities.

Traction motors remain the foundational product category within the market. These motors convert electrical energy into mechanical force and directly influence train performance characteristics such as acceleration, speed, efficiency, and reliability. AC induction motors currently dominate many applications because of their proven reliability and operational efficiency. However, permanent magnet synchronous motors are gaining traction due to their higher power density, improved efficiency, and reduced maintenance requirements. As operators seek greater energy savings and lower lifecycle costs, advanced motor technologies are expected to capture increasing market share.

Power converters and inverters represent another major segment. These components regulate electrical power flow between energy sources and traction systems, ensuring efficient operation under varying load conditions. The transition toward silicon carbide semiconductor technologies is creating substantial opportunities within this segment. Silicon carbide-based converters offer superior efficiency, reduced weight, improved thermal performance, and lower energy losses compared with conventional solutions.

Transformers continue to play a critical role in electrified rail networks by adapting power supply characteristics to propulsion system requirements. While transformer technology is relatively mature, innovation continues through lightweight materials, improved cooling systems, and enhanced energy efficiency designs. Future transformer development is expected to focus on reducing weight and improving compatibility with digital monitoring systems.

Energy storage systems are emerging as one of the fastest-growing product segments. Battery technologies are increasingly being integrated into propulsion architectures to support regenerative braking, hybrid operations, and battery-electric train applications. As battery costs decline and performance improves, energy storage systems are expected to become a more significant component of propulsion platforms.

Software and digital services are rapidly increasing their contribution to industry revenue. Historically, propulsion suppliers generated most of their income through hardware sales. Today, operators increasingly demand digital monitoring platforms, predictive maintenance solutions, performance analytics services, and remote diagnostics capabilities. These services create recurring revenue opportunities while improving customer retention and long-term profitability.

Maintenance, repair, and overhaul services constitute another substantial segment. Railway propulsion systems operate under demanding conditions and require regular servicing throughout their lifecycle. Long-term service agreements are becoming increasingly common as operators seek predictable maintenance costs and guaranteed performance levels. Service contracts often extend for decades, providing suppliers with stable revenue streams beyond initial equipment sales.

Retrofit and modernization services are also gaining importance. Many rail operators manage aging fleets that remain structurally sound but utilize outdated propulsion technologies. Modernization programs allow operators to improve efficiency, reliability, and regulatory compliance without replacing entire vehicles. This segment is expected to grow significantly as sustainability objectives encourage asset life extension strategies.

Looking toward 2035, software-enabled services, energy storage solutions, predictive maintenance platforms, and propulsion modernization programs are expected to experience the strongest growth. While traditional hardware segments will remain essential, future market expansion will increasingly be driven by integrated solutions that combine physical equipment with digital intelligence and lifecycle support services.

End-User Industry Analysis

The Railway Propulsion Systems Market serves a diverse range of end users, each with unique operational requirements, investment priorities, regulatory obligations, and performance expectations. Understanding these customer segments is essential because propulsion system specifications increasingly vary according to specific transportation applications.

Urban transit operators represent one of the largest end-user groups. Metro systems, light rail networks, tramways, and suburban commuter rail services require propulsion technologies optimized for frequent acceleration and braking cycles, high passenger volumes, and dense operating schedules. Energy efficiency is particularly important within urban environments because trains often operate continuously throughout the day. Regenerative braking capabilities, compact propulsion architectures, and advanced energy management systems are becoming critical purchasing criteria for transit authorities worldwide.

High-speed rail operators form another strategically important segment. These operators require propulsion systems capable of sustaining high velocities while maintaining reliability, passenger comfort, and operational efficiency. High-speed applications place significant demands on traction motors, power electronics, cooling systems, and control software. As countries expand high-speed rail networks to improve connectivity and reduce aviation-related emissions, demand for advanced high-performance propulsion technologies is expected to increase significantly.

Freight railway operators have distinct requirements that differ substantially from passenger transportation providers. Freight locomotives must deliver high tractive effort, durability, and operational reliability under heavy-load conditions. Energy efficiency remains important, but propulsion systems must also withstand harsh environmental conditions and extended operating cycles. The growth of sustainable logistics strategies is encouraging freight operators to invest in electrified and hybrid propulsion technologies capable of reducing fuel consumption and emissions.

Regional and intercity passenger rail operators represent another important customer segment. These operators often manage routes that combine urban, suburban, and rural environments. Flexibility is therefore a key requirement. Hybrid propulsion systems, battery-electric solutions, and hydrogen-powered trains are increasingly attractive for routes where complete network electrification may not be economically justified.

Industrial railway operators also contribute to market demand. Mining companies, port authorities, manufacturing facilities, and logistics hubs frequently operate dedicated rail systems requiring specialized propulsion solutions. These applications often prioritize durability, low maintenance requirements, and operational reliability over passenger-oriented performance characteristics.

Government agencies and transportation authorities play a significant role as indirect end users because they frequently influence procurement decisions through infrastructure planning, regulatory frameworks, and public funding programs. Their priorities increasingly emphasize sustainability, energy efficiency, safety, and long-term operational value.

Customer expectations are evolving rapidly across all end-user segments. Historically, propulsion procurement focused primarily on performance and reliability. Today, operators increasingly evaluate digital capabilities, predictive maintenance functionality, cybersecurity readiness, environmental performance, and lifecycle economics. This shift is encouraging suppliers to adopt more customer-centric product development strategies.

Looking toward 2035, end-user requirements are expected to become increasingly sophisticated. Autonomous train operations, integrated mobility platforms, advanced analytics, and sustainable energy systems will likely become standard expectations rather than optional features. Suppliers capable of anticipating these evolving customer needs will be best positioned to secure long-term competitive advantages.

Competitive Environment and Strategic Positioning

The Railway Propulsion Systems Market operates within a highly competitive environment characterized by technological specialization, long product lifecycles, significant capital requirements, and complex customer relationships. Competition extends beyond product performance and increasingly encompasses digital capabilities, lifecycle services, sustainability credentials, and ecosystem partnerships.

Industry structure is relatively concentrated because railway propulsion technologies require substantial engineering expertise, extensive certification processes, and long-term reliability validation. These barriers create a competitive landscape dominated by established technology providers with decades of experience in rail transportation systems. However, the industry is also witnessing the emergence of specialized technology firms focusing on software platforms, power electronics, battery technologies, and hydrogen propulsion solutions.

Competitive intensity is increasing as railway modernization programs expand globally. Growing demand attracts new participants while existing players seek to protect market share through innovation, partnerships, and service expansion. As a result, differentiation strategies are becoming increasingly sophisticated and multidimensional.

Technology leadership remains one of the most important sources of competitive advantage. Companies capable of delivering superior energy efficiency, reliability, digital integration, and operational performance can secure premium pricing and stronger customer loyalty. Investments in silicon carbide semiconductors, advanced traction motors, artificial intelligence, and energy management systems are increasingly influencing competitive positioning.

Lifecycle support capabilities represent another critical differentiator. Railway operators prefer suppliers capable of supporting assets throughout decades of operation. Long-term maintenance contracts, predictive analytics services, spare parts management, and modernization programs strengthen customer relationships while generating recurring revenue streams. Consequently, many propulsion providers are evolving from equipment manufacturers into lifecycle service partners.

Strategic partnerships are becoming increasingly important. Collaboration between propulsion suppliers, rolling stock manufacturers, software developers, infrastructure providers, and energy companies enables the development of integrated transportation solutions. These partnerships accelerate innovation, reduce development costs, and improve market access.

Sustainability credentials are also influencing competitive dynamics. Operators and government agencies increasingly prioritize suppliers capable of supporting decarbonization objectives. Companies offering energy-efficient technologies, alternative propulsion solutions, and environmentally responsible manufacturing practices may gain advantages during procurement processes.

Digital transformation is reshaping competitive boundaries. Traditional mechanical engineering expertise remains important, but software capabilities are becoming equally critical. Suppliers that successfully integrate digital monitoring, predictive maintenance, cybersecurity, and data analytics into propulsion platforms are creating new sources of value for customers.

Market positioning strategies vary considerably. Some companies focus on high-performance premium solutions for high-speed rail and advanced transit systems. Others emphasize cost-effective offerings for emerging markets or retrofit opportunities. The most successful organizations often combine technological innovation with strong service capabilities and global support networks.

Through 2035, competitive success will increasingly depend on the ability to deliver integrated solutions that combine hardware excellence, digital intelligence, sustainability performance, and lifecycle value. Organizations that adapt to these evolving competitive requirements are likely to strengthen their market positions as industry transformation accelerates

Regional dynamics play a decisive role in shaping demand patterns, investment priorities, technology adoption rates, and competitive opportunities within the Railway Propulsion Systems Market. While global sustainability and transportation modernization trends influence all regions, each geography exhibits distinct growth drivers and risk factors.

North America remains a strategically important market due to ongoing investments in freight rail modernization, urban transit expansion, and passenger rail development. The region possesses one of the world's largest freight rail networks, creating sustained demand for locomotive propulsion upgrades and energy-efficient technologies. Growing environmental concerns and infrastructure investment initiatives are encouraging increased adoption of electrified and hybrid propulsion solutions. However, extensive reliance on diesel-powered freight operations presents both a challenge and a long-term opportunity for technology providers.

Europe represents one of the most technologically advanced railway markets globally. Strong environmental policies, mature rail infrastructure, and ambitious decarbonization objectives are driving continuous investment in propulsion modernization. High-speed rail expansion, cross-border rail connectivity initiatives, and aggressive railway electrification programs support demand for advanced propulsion systems. Europe is also emerging as a major center for hydrogen-powered train development and next-generation sustainable mobility solutions. Regulatory complexity remains a challenge, but long-term growth prospects remain highly favorable.

Asia-Pacific is expected to remain the largest and fastest-growing regional market through 2035. Rapid urbanization, population growth, infrastructure development, and government investment programs are creating enormous demand for rail transportation systems. Countries across the region continue expanding metro networks, high-speed rail corridors, suburban transit systems, and freight transportation infrastructure. Large-scale railway construction projects generate substantial opportunities for propulsion suppliers. Additionally, domestic manufacturing capabilities and growing technological expertise are strengthening regional competitiveness.

China continues to dominate regional demand because of its extensive high-speed rail network, urban transit expansion, and railway technology investments. India is emerging as another major growth engine due to ambitious railway modernization initiatives, electrification programs, and freight corridor development projects. Southeast Asian nations are also increasing investments in urban transportation systems to address congestion and economic growth requirements.

Latin America presents a mixed opportunity landscape. Urban transit expansion projects and freight transportation modernization initiatives are creating demand for advanced propulsion technologies. However, economic volatility, funding constraints, and political uncertainty can affect project timelines and investment decisions. Countries with strong infrastructure development agendas are likely to generate the most attractive opportunities.

The Middle East and Africa region remains relatively smaller but offers significant long-term potential. Several countries are investing heavily in railway infrastructure to support economic diversification, urban development, and regional connectivity objectives. Large-scale rail projects, particularly within Gulf economies, are creating opportunities for advanced propulsion systems. Africa's long-term growth potential is supported by increasing infrastructure investment and rising demand for efficient freight transportation networks.

Regional opportunities through 2035 will increasingly depend on government transportation strategies, sustainability commitments, economic development priorities, and infrastructure investment capacity. Asia-Pacific is expected to remain the primary growth engine, while Europe will continue leading technological innovation. North America, Latin America, and the Middle East & Africa will offer selective high-value opportunities tied to modernization and expansion initiatives.

Regional Market Analysis

Regional dynamics play a decisive role in shaping demand patterns, investment priorities, technology adoption rates, and competitive opportunities within the Railway Propulsion Systems Market. While global sustainability and transportation modernization trends influence all regions, each geography exhibits distinct growth drivers and risk factors.

North America remains a strategically important market due to ongoing investments in freight rail modernization, urban transit expansion, and passenger rail development. The region possesses one of the world's largest freight rail networks, creating sustained demand for locomotive propulsion upgrades and energy-efficient technologies. Growing environmental concerns and infrastructure investment initiatives are encouraging increased adoption of electrified and hybrid propulsion solutions. However, extensive reliance on diesel-powered freight operations presents both a challenge and a long-term opportunity for technology providers.

Europe represents one of the most technologically advanced railway markets globally. Strong environmental policies, mature rail infrastructure, and ambitious decarbonization objectives are driving continuous investment in propulsion modernization. High-speed rail expansion, cross-border rail connectivity initiatives, and aggressive railway electrification programs support demand for advanced propulsion systems. Europe is also emerging as a major center for hydrogen-powered train development and next-generation sustainable mobility solutions. Regulatory complexity remains a challenge, but long-term growth prospects remain highly favorable.

Asia-Pacific is expected to remain the largest and fastest-growing regional market through 2035. Rapid urbanization, population growth, infrastructure development, and government investment programs are creating enormous demand for rail transportation systems. Countries across the region continue expanding metro networks, high-speed rail corridors, suburban transit systems, and freight transportation infrastructure. Large-scale railway construction projects generate substantial opportunities for propulsion suppliers. Additionally, domestic manufacturing capabilities and growing technological expertise are strengthening regional competitiveness.

China continues to dominate regional demand because of its extensive high-speed rail network, urban transit expansion, and railway technology investments. India is emerging as another major growth engine due to ambitious railway modernization initiatives, electrification programs, and freight corridor development projects. Southeast Asian nations are also increasing investments in urban transportation systems to address congestion and economic growth requirements.

Latin America presents a mixed opportunity landscape. Urban transit expansion projects and freight transportation modernization initiatives are creating demand for advanced propulsion technologies. However, economic volatility, funding constraints, and political uncertainty can affect project timelines and investment decisions. Countries with strong infrastructure development agendas are likely to generate the most attractive opportunities.

The Middle East and Africa region remains relatively smaller but offers significant long-term potential. Several countries are investing heavily in railway infrastructure to support economic diversification, urban development, and regional connectivity objectives. Large-scale rail projects, particularly within Gulf economies, are creating opportunities for advanced propulsion systems. Africa's long-term growth potential is supported by increasing infrastructure investment and rising demand for efficient freight transportation networks.

Regional opportunities through 2035 will increasingly depend on government transportation strategies, sustainability commitments, economic development priorities, and infrastructure investment capacity. Asia-Pacific is expected to remain the primary growth engine, while Europe will continue leading technological innovation. North America, Latin America, and the Middle East & Africa will offer selective high-value opportunities tied to modernization and expansion initiatives.

Supply Chain, Manufacturing, and Trade Analysis

The Railway Propulsion Systems Market relies on one of the most sophisticated industrial supply chains within the transportation sector. The complexity arises from the integration of advanced electrical engineering, precision manufacturing, software development, power electronics, metallurgy, and safety-critical system design. As railway operators increasingly demand higher efficiency, lower emissions, and enhanced digital capabilities, supply chain resilience has become a strategic priority rather than merely an operational consideration.

The production ecosystem begins with the sourcing of critical raw materials such as copper, aluminum, electrical steel, silicon wafers, specialty alloys, rare earth elements, insulation materials, and advanced polymers. Copper remains particularly important because traction motors, transformers, converters, and electrical distribution systems require significant quantities of high-conductivity materials. Any disruption in copper markets can directly affect production costs and project timelines. Similarly, rare earth materials are becoming increasingly important because permanent magnet motors deliver higher efficiency and power density compared to traditional motor technologies.

Component manufacturing forms the second layer of the ecosystem. This stage includes production of traction motors, power converters, inverters, transformers, cooling systems, braking equipment, sensors, control units, and onboard software systems. The increasing adoption of silicon carbide semiconductors has elevated the importance of advanced electronics manufacturing capabilities. Unlike traditional industrial equipment, railway propulsion systems must meet extremely demanding reliability and safety requirements, creating lengthy qualification and testing procedures throughout the supply chain.

System integration represents one of the highest value-added stages. Propulsion systems must function flawlessly within complex railway environments where reliability, safety, and operational continuity are paramount. Integration activities involve combining hardware, electronics, software, communication systems, and safety protocols into a unified platform capable of operating under diverse environmental and operational conditions. This stage increasingly depends on digital engineering tools, simulation technologies, and virtual testing platforms.

Trade patterns within the industry are becoming more regionalized. Geopolitical uncertainty, supply chain disruptions, semiconductor shortages, and transportation bottlenecks have encouraged manufacturers to diversify sourcing strategies and localize production where possible. Governments are also encouraging domestic manufacturing capabilities to reduce dependence on foreign suppliers for critical transportation infrastructure technologies.

International trade remains essential because no single country possesses all the resources, technologies, and manufacturing expertise required for complete propulsion system production. Advanced semiconductors may originate in one region, rare earth materials in another, and final assembly operations in a third. Consequently, global trade relationships continue to influence cost structures, lead times, and competitive positioning.

Supply chain resilience has emerged as a defining strategic objective. Manufacturers increasingly maintain multiple sourcing channels, establish regional manufacturing hubs, invest in inventory management technologies, and develop supplier diversification strategies. Digital supply chain monitoring tools are also becoming more prevalent, enabling real-time visibility into supplier performance, inventory levels, logistics bottlenecks, and potential disruption risks.

Looking toward 2035, supply chains are expected to become more digitally integrated, regionally diversified, and sustainability focused. Companies that successfully combine manufacturing excellence with resilient sourcing strategies and intelligent supply chain management will gain significant competitive advantages in an increasingly complex global market.

Investment and Funding Landscape

Investment activity within the Railway Propulsion Systems Market reflects broader trends in transportation modernization, energy transition, digital transformation, and infrastructure development. Capital flows are increasingly directed toward technologies that improve efficiency, reduce emissions, enhance reliability, and support long-term mobility objectives. As governments and private investors prioritize sustainable transportation, railway propulsion systems are emerging as an attractive investment category with strong long-term growth fundamentals.

Infrastructure spending remains the primary source of market investment. National governments worldwide continue allocating substantial budgets to railway modernization, urban transit expansion, freight corridor development, and high-speed rail projects. These infrastructure initiatives create direct demand for propulsion systems while supporting broader ecosystem growth. Unlike many industrial markets that depend heavily on short-term economic cycles, railway propulsion investments often benefit from multi-decade infrastructure planning horizons.

Capital expenditure trends indicate growing investment in electrification projects. Railway operators increasingly recognize the long-term economic and environmental benefits of electric propulsion technologies. Electrification investments not only improve operational efficiency but also reduce dependence on fossil fuels and support national carbon reduction objectives. Consequently, propulsion suppliers focused on electric traction technologies are attracting significant investment attention.

Digitalization is creating a new wave of funding opportunities. Investors are increasingly interested in companies developing predictive maintenance platforms, fleet optimization software, intelligent energy management systems, cybersecurity solutions, and artificial intelligence applications for rail operations. These technologies generate recurring revenue opportunities while enhancing operational value for customers. As a result, software-oriented railway technology firms are attracting increasing levels of strategic investment.

Alternative propulsion technologies represent another major investment theme. Battery-electric trains, hydrogen-powered locomotives, hybrid propulsion architectures, and advanced energy storage systems are receiving growing attention from both public and private investors. While some of these technologies remain in relatively early stages of commercialization, their potential to support zero-emission transportation objectives is generating substantial funding activity.

Strategic investments from industrial companies are also reshaping the competitive landscape. Large transportation technology providers are expanding their capabilities through acquisitions, joint ventures, and technology partnerships. These investments aim to strengthen positions in emerging areas such as power electronics, battery technologies, software platforms, and digital railway solutions.

Mergers and acquisitions are expected to remain active through 2035. Industry participants increasingly seek access to specialized technologies, intellectual property portfolios, engineering talent, and regional market presence. Consolidation may accelerate as digital capabilities become more important and competitive pressures intensify.

Institutional investors are demonstrating growing interest in railway-related infrastructure assets because of their long-term stability, predictable cash flows, and alignment with sustainability objectives. Pension funds, sovereign wealth funds, infrastructure funds, and long-term capital providers increasingly view rail transportation as a strategic investment category capable of delivering resilient returns.

The future investment outlook remains highly favorable. Continued urbanization, decarbonization efforts, freight transportation growth, and infrastructure modernization are expected to sustain capital inflows into the sector. Companies aligned with electrification, digitalization, alternative energy technologies, and lifecycle service models are likely to attract the greatest investment interest over the next decade.

Regulatory, ESG, and Sustainability Factors

Regulatory frameworks, environmental priorities, and ESG considerations are becoming central forces shaping the Railway Propulsion Systems Market. Increasing pressure to reduce transportation-related emissions, improve energy efficiency, and enhance infrastructure sustainability is influencing procurement decisions, technology development strategies, and long-term investment priorities across the industry.

Government policy remains one of the most influential factors affecting market development. Many countries have established ambitious transportation decarbonization targets that prioritize rail as a lower-emission alternative to road and air transport. These policies encourage railway electrification, investment in sustainable propulsion technologies, and modernization of aging transportation infrastructure. In many cases, regulatory support directly influences technology adoption rates and investment decisions.

Safety regulations remain among the most stringent in the transportation sector. Railway propulsion systems must comply with comprehensive standards governing reliability, operational safety, electromagnetic compatibility, cybersecurity, passenger protection, and environmental performance. Compliance requirements vary across regions, creating complexity for manufacturers operating internationally. However, strict regulatory standards also create barriers to entry that protect established industry participants.

Environmental regulations are becoming increasingly demanding. Governments and transportation authorities are imposing stricter emissions requirements, energy efficiency targets, and sustainability reporting obligations. These measures are accelerating the transition away from diesel-powered systems while encouraging investment in electric, battery-electric, hydrogen, and hybrid propulsion technologies. Environmental compliance is no longer viewed solely as a regulatory obligation. It is increasingly recognized as a competitive advantage.

ESG considerations have moved from peripheral concerns to board-level strategic priorities. Investors, customers, regulators, and communities increasingly evaluate companies based on environmental performance, social responsibility, and governance practices. Railway propulsion manufacturers are responding by improving energy efficiency, reducing manufacturing emissions, enhancing supply chain transparency, and strengthening ethical sourcing practices.

The environmental benefits of rail transportation provide a strong foundation for industry growth. Rail systems generally consume less energy per passenger kilometer or freight ton-kilometer compared with alternative transportation modes. As climate commitments intensify globally, policymakers are expected to allocate greater resources toward rail infrastructure development and modernization. This creates favorable long-term conditions for propulsion technology providers.

Supply chain sustainability is receiving increasing attention. Manufacturers are being asked to demonstrate responsible sourcing of critical materials, particularly rare earth elements, metals, and semiconductor components. Transparency, traceability, and environmental stewardship are becoming important procurement criteria within both public and private sector contracts.

Social considerations also influence market dynamics. Railway investments often support economic development, urban mobility, employment creation, and regional connectivity objectives. Consequently, propulsion technologies that contribute to reliable, accessible, and efficient transportation systems align with broader social development goals.

Looking toward 2035, ESG performance is expected to become deeply integrated into procurement processes, investment decisions, and competitive positioning. Companies capable of combining technological innovation with strong sustainability credentials, transparent governance practices, and responsible supply chain management will be best positioned to capitalize on evolving stakeholder expectations and regulatory requirements.

Future Opportunities and Emerging Business Models

The Railway Propulsion Systems Market is entering a period where future growth opportunities will increasingly be driven by innovation, digital services, alternative energy solutions, and evolving customer expectations. While traditional equipment sales will remain important, new business models are emerging that have the potential to fundamentally reshape revenue generation, customer relationships, and competitive dynamics through 2035.

One of the most significant opportunities lies in the expansion of propulsion-as-a-service models. Historically, railway operators purchased propulsion equipment as capital assets and managed maintenance internally. Increasingly, suppliers are offering long-term service agreements that bundle equipment, maintenance, software updates, predictive analytics, and performance guarantees into integrated lifecycle solutions. This model provides customers with predictable costs while creating recurring revenue streams for suppliers.

Digital services represent another transformative opportunity. Modern propulsion systems generate enormous volumes of operational data that can be analyzed to improve performance, reduce downtime, optimize energy consumption, and extend asset lifecycles. Suppliers capable of monetizing data analytics, predictive maintenance, remote diagnostics, and operational intelligence platforms may unlock entirely new revenue categories that extend far beyond traditional hardware sales.

Alternative propulsion technologies are creating substantial growth potential. Hydrogen-powered trains, battery-electric systems, and hybrid propulsion platforms are expanding addressable market opportunities, particularly in regions where full electrification remains economically challenging. As governments pursue aggressive emissions reduction targets, demand for zero-emission propulsion technologies is expected to accelerate significantly.

Railway modernization programs represent another major opportunity area. Many rail operators continue operating fleets equipped with aging propulsion technologies. Retrofitting these vehicles with modern traction systems, advanced electronics, and intelligent monitoring platforms can deliver substantial efficiency improvements at a fraction of the cost of fleet replacement. This creates a large and relatively stable aftermarket opportunity.

Energy management services may emerge as a major business segment. Railway operators face increasing pressure to manage electricity costs and improve sustainability performance. Propulsion providers that offer integrated energy optimization solutions, regenerative braking management systems, and intelligent power consumption analytics can create meaningful customer value while expanding service revenues.

Autonomous and semi-autonomous train operations may eventually create additional opportunities. Advanced propulsion systems integrated with automation technologies, AI-driven controls, and intelligent traffic management platforms could significantly improve network efficiency and safety. Suppliers capable of supporting this transition may gain early-mover advantages in future railway ecosystems.

Emerging markets remain largely underpenetrated relative to long-term transportation needs. Urbanization, industrialization, and infrastructure development across Asia, Africa, Latin America, and parts of the Middle East are expected to create substantial demand for rail transportation systems. These regions offer opportunities for both new infrastructure projects and technology transfer initiatives.

By 2035, the most successful business models are likely to combine hardware excellence with software intelligence, long-term service relationships, sustainability solutions, and operational performance optimization. The market is gradually transitioning from a product-focused industry toward a comprehensive mobility technology ecosystem where value creation extends throughout the entire asset lifecycle.

Strategic Outlook Through 2035

The Railway Propulsion Systems Market is expected to undergo one of the most significant periods of transformation in its history between now and 2035. The convergence of electrification, digitalization, sustainability imperatives, alternative energy technologies, and intelligent transportation systems is reshaping both market structure and competitive dynamics. Organizations that recognize these structural shifts early will be best positioned to capture long-term growth opportunities.

The most likely industry transformation scenario involves the continued decline of conventional diesel propulsion systems in favor of electric, battery-electric, hydrogen, and hybrid technologies. While diesel-powered fleets will remain operational in certain regions and applications, new investments are increasingly being directed toward lower-emission alternatives. This transition is expected to accelerate as governments implement stricter environmental regulations and transportation operators pursue sustainability objectives.

Digital intelligence will become a core component of propulsion system value. By 2035, propulsion platforms are expected to function as connected, data-generating assets integrated into broader railway management ecosystems. Artificial intelligence, predictive maintenance, digital twins, cloud analytics, and autonomous operational support systems will likely become standard features rather than premium options. The ability to convert operational data into actionable business insights will emerge as a major source of competitive advantage.

Energy efficiency will remain a dominant strategic priority. Rising electricity demand, grid modernization efforts, and sustainability commitments will encourage adoption of advanced power electronics, regenerative braking systems, intelligent energy management platforms, and lightweight propulsion architectures. Future procurement decisions will increasingly emphasize total lifecycle efficiency rather than initial equipment cost.

Regional growth patterns will continue evolving. Asia-Pacific is expected to remain the largest growth engine because of ongoing urbanization, infrastructure development, and railway expansion programs. Europe will likely maintain leadership in sustainability-focused innovation, while North America will continue investing in freight modernization and selective passenger rail expansion. Emerging economies across Africa, Latin America, and the Middle East may generate significant long-term opportunities as transportation infrastructure investments accelerate.

Competitive dynamics are expected to shift toward ecosystem-based competition. Success will increasingly depend on partnerships among propulsion suppliers, rolling stock manufacturers, software developers, infrastructure operators, and energy providers. Organizations capable of delivering integrated solutions rather than standalone products will likely achieve stronger market positions.

Several key success factors will define industry leadership through 2035. Continuous investment in advanced propulsion technologies, strong digital capabilities, resilient supply chains, lifecycle service expertise, sustainability leadership, and global customer support networks will become essential competitive requirements. Companies that fail to adapt to these evolving expectations risk losing relevance as customer requirements become increasingly sophisticated.

From an executive perspective, strategic planning should focus on long-term technology positioning rather than short-term market fluctuations. The market's fundamental growth drivers, including urbanization, decarbonization, infrastructure modernization, and transportation electrification, remain highly favorable. These trends provide a strong foundation for sustained expansion over the next decade.

The long-term outlook through 2035 remains overwhelmingly positive. Railway propulsion systems are evolving from traditional engineering products into intelligent mobility technologies that support sustainable transportation, operational efficiency, and digital transformation. As governments, operators, and investors continue prioritizing railway infrastructure development, propulsion technologies will remain at the center of global transportation modernization efforts, creating substantial opportunities for innovation,

Top 10 Industry Trends Reshaping the Railway Propulsion Systems Market

1. Rapid Electrification of Railway Networks

Railway electrification is emerging as one of the most influential trends shaping the future of global transportation infrastructure. Governments, railway operators, and transportation planners increasingly recognize that electrified rail systems provide substantial advantages in energy efficiency, environmental performance, operating costs, and long-term sustainability. As countries pursue aggressive carbon reduction targets and seek alternatives to fossil fuel-dependent transportation systems, electrification has become a central pillar of railway modernization strategies.

The economic rationale behind electrification is becoming increasingly compelling. Electric propulsion systems typically offer higher energy conversion efficiency compared with diesel-powered alternatives, resulting in lower operating expenses over the lifetime of railway assets. Electric trains also require fewer moving mechanical components, reducing maintenance requirements and improving fleet reliability. These advantages are particularly important as operators seek to optimize asset utilization and improve service quality.

Urbanization is further accelerating electrification investments. Growing metropolitan populations require transportation systems capable of moving large numbers of passengers efficiently and sustainably. Electrified metro systems, commuter rail networks, and high-capacity transit corridors are becoming essential infrastructure assets for rapidly expanding cities. Consequently, railway operators are prioritizing propulsion systems designed specifically for intensive urban operations.

Technological advancements are making electrification more attractive than ever. Modern traction motors, advanced power electronics, regenerative braking systems, and intelligent energy management platforms significantly improve operational efficiency while reducing energy consumption. The integration of digital monitoring systems further enhances the value proposition by enabling predictive maintenance and performance optimization.

Looking toward 2035, railway electrification is expected to expand beyond traditional passenger rail applications. Freight transportation corridors, regional rail systems, and cross-border logistics networks will increasingly adopt electrified propulsion technologies. As renewable energy generation expands globally, electrified railways may also become more environmentally sustainable over time, creating additional momentum for investment and adoption.

Ultimately, electrification represents more than a technology upgrade. It reflects a structural transformation of the transportation sector that aligns economic efficiency, environmental responsibility, and long-term mobility objectives. Propulsion system manufacturers capable of supporting large-scale electrification programs will likely benefit from one of the strongest growth trends in the railway industry.

2. Expansion of Battery-Electric Train Technologies

Battery-electric train technology is rapidly transitioning from a niche innovation into a commercially viable solution for a growing range of railway applications. This trend is being driven by improvements in battery performance, declining energy storage costs, increasing environmental regulations, and the practical challenges associated with full network electrification. As a result, battery-powered propulsion systems are attracting significant attention from railway operators worldwide.

One of the primary advantages of battery-electric trains is their ability to operate without continuous overhead electrical infrastructure. Many regional rail corridors, branch lines, and rural routes do not justify the substantial capital expenditure required for complete electrification. Battery-powered trains provide a cost-effective alternative by enabling zero-emission operations without extensive infrastructure investments.

Advances in lithium-ion batteries, solid-state battery research, thermal management technologies, and charging systems are improving the commercial viability of battery-electric rail transportation. Modern battery systems offer greater energy density, longer operational range, faster charging capabilities, and improved lifecycle performance compared with earlier generations of technology. These improvements are expanding the range of operational scenarios where battery propulsion can be effectively deployed.

Battery-electric trains also support broader energy transition objectives. Many operators are exploring ways to integrate renewable energy sources into railway operations. Battery systems can help balance energy demand, store regenerative braking energy, and improve overall network energy efficiency. These capabilities provide both environmental and economic benefits.

Another important factor supporting adoption is regulatory pressure. Governments increasingly seek to eliminate diesel-powered transportation assets from their networks. Battery-electric trains offer a practical pathway toward compliance with stricter emissions regulations while minimizing disruption to existing railway operations.

Looking ahead, battery-electric propulsion is expected to become increasingly important in regional passenger transportation, light rail systems, industrial rail operations, and secondary freight corridors. While battery technology may not replace conventional electrification for all applications, it will likely play a critical role within future multimodal propulsion ecosystems.

By 2035, battery-electric rail solutions may represent one of the most significant growth segments within the propulsion market, particularly in regions where infrastructure investment budgets remain constrained but environmental objectives continue to intensify.

3. Growth of Hydrogen Rail Propulsion

Hydrogen propulsion is emerging as one of the most strategically important developments within the railway sector. Although still at an earlier stage of commercialization compared with electric traction systems, hydrogen-powered trains offer a compelling solution for non-electrified routes seeking zero-emission transportation alternatives. This trend is attracting growing attention from governments, infrastructure developers, railway operators, and technology investors.

The primary appeal of hydrogen propulsion lies in its ability to eliminate direct emissions while avoiding the need for extensive electrification infrastructure. Many regional and rural rail networks operate across large geographic areas where installing overhead power systems may be economically challenging. Hydrogen fuel cell trains can provide similar environmental benefits to electric trains without requiring major modifications to existing rail infrastructure.

Hydrogen-powered propulsion systems generate electricity through electrochemical reactions rather than combustion. This process produces only water vapor as a byproduct, making it an attractive option for operators pursuing aggressive sustainability targets. As governments strengthen carbon reduction commitments, hydrogen technology is increasingly viewed as an important component of future transportation strategies.

Technological progress is helping improve the commercial viability of hydrogen rail systems. Fuel cell efficiency, hydrogen storage technologies, refueling infrastructure, and system reliability continue to advance. At the same time, investments in green hydrogen production are expanding, potentially reducing fuel costs and improving environmental performance.

Hydrogen propulsion also offers operational advantages in certain applications. Compared with battery-electric trains, hydrogen-powered trains can often achieve longer operating ranges and faster refueling times. These characteristics make them particularly attractive for long-distance regional services and freight operations where extended operational flexibility is required.

However, challenges remain. Hydrogen production costs, infrastructure development requirements, storage complexity, and safety considerations continue to influence adoption rates. Nevertheless, ongoing technological innovation and policy support are gradually addressing these barriers.

Through 2035, hydrogen propulsion is expected to evolve from demonstration projects into broader commercial deployment. While it may not replace electrification in all circumstances, hydrogen technology is likely to become a significant component of the global railway propulsion landscape, particularly in regions seeking sustainable alternatives for non-electrified rail corridors.

4. Digitalization of Propulsion Management

Digitalization is fundamentally transforming the way railway propulsion systems are designed, operated, maintained, and optimized. Historically, propulsion systems functioned primarily as mechanical and electrical assets with limited connectivity. Today, they are becoming intelligent digital platforms capable of generating, transmitting, and analyzing vast amounts of operational data in real time.

The driving force behind this transformation is the increasing need for operational efficiency, asset reliability, and cost optimization. Railway operators face mounting pressure to improve service quality while controlling expenses. Digital propulsion management systems provide valuable insights into equipment performance, energy consumption, maintenance requirements, and operational efficiency.

Modern propulsion platforms incorporate sensors throughout critical components such as traction motors, converters, transformers, cooling systems, and braking equipment. These sensors continuously collect data regarding temperature, vibration, power consumption, electrical performance, and mechanical condition. Advanced software platforms analyze this information to identify performance anomalies and emerging maintenance requirements.

Digitalization also supports predictive maintenance strategies. Instead of relying solely on fixed maintenance schedules, operators can monitor actual equipment conditions and perform maintenance when needed. This approach reduces unnecessary maintenance activities, minimizes downtime, and improves asset utilization.

Energy management is another area benefiting significantly from digitalization. Real-time monitoring systems allow operators to optimize energy consumption, improve regenerative braking performance, and reduce electricity costs. Given the increasing importance of sustainability and energy efficiency, these capabilities are becoming critical competitive advantages.

Cloud computing, edge computing, and industrial Internet of Things technologies are accelerating adoption by making large-scale data analysis more practical and cost effective. Integration with broader railway management systems further enhances operational visibility across entire transportation networks.

Looking toward 2035, digital propulsion management will likely become a standard feature rather than a premium capability. Future propulsion systems will increasingly function as intelligent, connected assets capable of continuously optimizing performance, supporting autonomous operations, and contributing to broader smart transportation ecosystems.

5. Artificial Intelligence Integration