-

이메일 문의

- 주요 보고서

Housing Cost Burden in the EU Continues to Ease Through 2027, Yet Urban Residents Still Face the Greatest Affordability Pressure

게시일 22 June, 2026

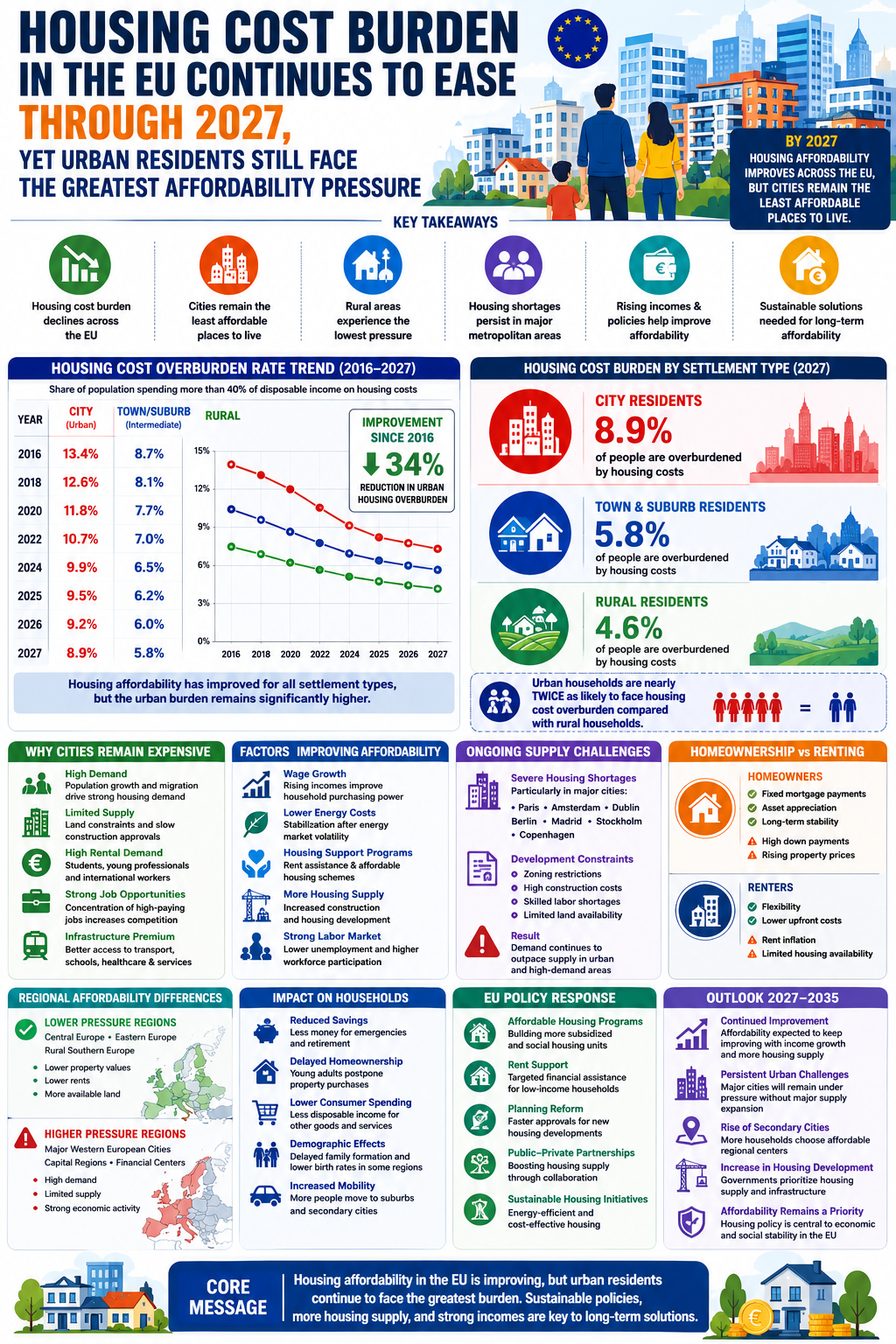

Across the European Union, housing affordability remains one of the most important economic and social challenges facing households. Although the share of people experiencing severe housing cost burdens has gradually declined over the past decade, the pressure of rising rents, elevated property prices, and constrained housing supply continues to weigh heavily on urban residents.

By 2027, the European housing market presents a mixed picture. Housing cost overburden rates have improved compared with pre-pandemic levels, reflecting stronger labor markets, rising wages, and policy interventions aimed at improving access to housing. However, affordability remains unevenly distributed, with city residents consistently experiencing significantly greater financial strain than those living in towns, suburbs, and rural communities.

The latest trends indicate that while progress has been made in reducing housing-related financial stress across the EU, structural housing shortages in major metropolitan areas continue to challenge policymakers and households alike.

Housing Cost Burden Shows Sustained Improvement Through 2027

The housing cost overburden rate measures the share of people living in households where total housing expenses exceed 40% of disposable income. This indicator remains one of the most widely used measures of housing affordability across Europe.

In 2016, approximately 13.4% of city residents across the EU were spending more than 40% of their disposable income on housing costs. By 2024, this figure had fallen to roughly 9.8%, representing a significant improvement in housing affordability.

Recent estimates suggest that by 2027 the burden among city residents has continued to decline modestly, reaching approximately 9.1%. Although this marks steady progress, nearly one in eleven urban residents still experiences severe housing affordability challenges.

A similar pattern can be observed in towns and suburban areas. The housing cost burden declined from around 10.3% in 2016 to 7.8% in 2024 and is estimated to have eased further to approximately 7.1% by 2027.

Rural regions continue to record the lowest housing cost pressures. The burden rate fell from roughly 8.5% in 2016 to 6.3% in 2024 and is projected to stand near 5.8% by 2027.

These improvements reflect several factors including stronger employment conditions, gradual wage growth, government housing assistance programs, expanded social housing initiatives, and increased attention to affordability challenges by national and local authorities.

Estimated EU Housing Cost Overburden Rate by Degree of Urbanization (2016–2027)

| Year | Cities (%) | Towns & Suburbs (%) | Rural Areas (%) |

| 2016 | 13.4 | 10.3 | 8.5 |

| 2017 | 13.1 | 10.0 | 8.2 |

| 2018 | 12.7 | 9.8 | 8.0 |

| 2019 | 12.3 | 9.4 | 7.8 |

| 2020 | 10.4 | 8.1 | 6.7 |

| 2021 | 10.8 | 8.4 | 6.9 |

| 2022 | 11.2 | 8.8 | 7.2 |

| 2023 | 10.5 | 8.2 | 6.7 |

| 2024 | 9.8 | 7.8 | 6.3 |

| 2025* | 9.5 | 7.5 | 6.1 |

| 2026* | 9.3 | 7.3 | 5.9 |

| 2027* | 9.1 | 7.1 | 5.8 |

*2025–2027 values represent trend-based estimates derived from recent EU housing market developments

.

Urban Areas Continue to Experience the Highest Housing Pressure

Despite the overall improvement in affordability indicators, cities remain substantially more expensive places to live than towns, suburbs, or rural areas.

The urban housing challenge is fundamentally driven by a mismatch between demand and supply. Europe's largest cities continue to attract workers, students, entrepreneurs, and international migrants seeking economic opportunities. At the same time, housing construction has struggled to keep pace with population growth in many metropolitan areas.

As a result, demand for housing continues to exceed available supply in numerous urban markets, pushing both rental and ownership costs higher.

Several factors continue to fuel urban housing demand:

- Population growth

- Internal migration toward economic centers

- International migration

- Expanding technology and service sectors

- University student populations

- Tourism-related housing demand

- Limited land availability

- Lengthy planning and permitting processes

The result is a persistent affordability gap between major cities and less densely populated regions.

Europe's Major Cities Remain Affordability Hotspots

Several European metropolitan areas continue to experience some of the highest housing cost pressures in the region.

Among the cities facing sustained affordability challenges are:

- Paris

- Amsterdam

- Dublin

- Berlin

- Madrid

- Stockholm

- Copenhagen

- Lisbon

- Vienna

- Brussels

In many of these locations, rental growth has outpaced wage growth over extended periods, making housing increasingly difficult to afford for younger households, low-income workers, and first-time buyers.

Housing shortages have become particularly visible in technology and innovation hubs where job creation has accelerated more rapidly than residential development.

Post-Pandemic Recovery Reshaped Housing Affordability

The COVID-19 pandemic represented a major turning point for European housing markets.

During 2020, emergency income support programs, mortgage payment relief measures, and rent protections helped cushion the immediate impact of economic disruption. As a result, housing cost burden indicators temporarily declined across much of Europe.

However, the post-pandemic recovery introduced new challenges.

Between 2021 and 2023, households faced:

- High inflation

- Rising energy bills

- Increased utility costs

- Supply chain disruptions

- Elevated construction expenses

- Sharp increases in mortgage interest rates

These factors created renewed affordability pressures despite rising employment levels.

Fortunately, housing burden rates generally remained below pre-pandemic peaks, suggesting that labor market resilience and government support measures helped prevent a widespread housing affordability crisis.

Interest Rate Stabilization Brings Some Relief

One of the most significant developments between 2025 and 2027 has been the gradual stabilization of European interest rates.

After aggressive monetary tightening by the European Central Bank during the inflation surge of 2022–2024, borrowing conditions have become somewhat more predictable.

Although mortgage rates remain above the ultra-low levels seen before 2022, the stabilization of financing costs has improved confidence among homebuyers and developers.

This has contributed to:

- Increased residential construction activity

- Higher housing market liquidity

- Improved mortgage affordability

- More stable housing price growth

Nevertheless, affordability challenges remain particularly severe in supply-constrained urban markets.

Rural Areas Maintain a Significant Affordability Advantage

Throughout the entire 2016–2027 period, rural households consistently reported the lowest housing cost burden.

Several structural advantages explain this trend:

- Lower property prices

- Lower monthly rents

- Greater land availability

- Lower population density

- Reduced competition among buyers

- More flexible housing supply

The rise of remote and hybrid work arrangements has further strengthened the appeal of rural living.

Many households that previously needed to live near major employment centers now have greater flexibility in choosing where they reside. As a result, some rural and semi-rural communities have experienced population growth for the first time in decades.

While rural areas often face challenges related to transportation, healthcare access, and employment opportunities, they continue to offer significantly more affordable housing options compared with Europe's largest cities.

Housing Supply Remains the Core Challenge

Housing experts increasingly agree that Europe's affordability challenges are primarily supply-related.

Demand for housing has remained strong across much of the continent, but housing construction has frequently lagged behind demographic and economic growth.

Key barriers to housing supply include:

- Limited urban land availability

- Strict zoning regulations

- Lengthy permitting procedures

- Construction labor shortages

- Rising material costs

- Environmental compliance requirements

- Financing constraints for developers

Without substantial increases in residential construction, affordability gains may remain limited despite broader economic improvements.

Governments Expand Housing Policy Initiatives

Recognizing the importance of affordable housing, governments across Europe have intensified policy efforts between 2024 and 2027.

Common policy approaches include:

Affordable Housing Programs

Many countries have expanded social housing and subsidized housing initiatives aimed at lower-income households.

Accelerated Construction Approvals

Several municipalities have introduced streamlined planning processes designed to increase housing supply more rapidly.

First-Time Buyer Support

Governments continue to offer grants, tax incentives, and mortgage assistance programs to help younger households enter the housing market.

Urban Regeneration Projects

Large-scale redevelopment programs are transforming underutilized industrial and commercial areas into residential communities.

Public Transport Investments

Improved transport infrastructure is helping connect more affordable suburban locations with major employment centers, reducing pressure on city housing markets.

Demographic Trends Will Shape Future Housing Demand

The long-term outlook for European housing affordability will be heavily influenced by demographic developments.

Several structural trends are expected to affect housing markets through the next decade:

- Continued urbanization

- Aging populations

- International migration

- Smaller household sizes

- Increased single-person households

- Growing student populations

- Workforce mobility

- Climate-related migration patterns

These trends suggest that housing demand will remain strong, particularly in economically dynamic metropolitan regions.

Outlook for 2027 and Beyond

Looking beyond 2027, housing affordability is expected to remain one of Europe's defining socioeconomic issues.

The encouraging decline in housing cost burden rates demonstrates that meaningful progress is possible through a combination of economic growth, labor market strength, and targeted housing policies. However, the persistent gap between cities and rural areas highlights the ongoing challenge of balancing housing demand with available supply.

Urban residents continue to face the greatest affordability pressures, and housing shortages in major metropolitan areas remain a significant obstacle to inclusive economic growth. Ensuring access to affordable, high-quality housing will be critical for maintaining social cohesion, supporting labor mobility, and enhancing Europe's long-term competitiveness.

As the European Union moves further into the late 2020s, policymakers will increasingly focus on accelerating housing construction, modernizing planning systems, and expanding affordable housing programs. The success of these efforts will largely determine whether the recent improvements in housing affordability can be sustained and extended across all regions of Europe.

The overall trend through 2027 is positive. Yet for millions of Europeans living in major cities, housing affordability remains a daily challenge, making it one of the most important policy priorities for the decade ahead.

EU HOUSING COST BURDEN 2016–2027

Housing Affordability Improves Across Europe, Yet Cities Continue to Face the Greatest Pressure

Housing Cost Overburden Rate by Degree of Urbanization (% of Population Spending More Than 40% of Disposable Income on Housing)

| Year | Cities (%) | Towns and Suburbs (%) | Rural Areas (%) |

| 2016 | 13.4 | 10.3 | 8.5 |

| 2017 | 13.1 | 10.0 | 8.2 |

| 2018 | 12.7 | 9.8 | 8.0 |

| 2019 | 12.3 | 9.4 | 7.8 |

| 2020 | 10.4 | 8.1 | 6.7 |

| 2021 | 10.8 | 8.4 | 6.9 |

| 2022 | 11.2 | 8.8 | 7.2 |

| 2023 | 10.5 | 8.2 | 6.7 |

| 2024 | 9.8 | 7.8 | 6.3 |

| 2025* | 9.5 | 7.5 | 6.1 |

| 2026* | 9.3 | 7.3 | 5.9 |

| 2027* | 9.1 | 7.1 | 5.8 |

*2025–2027 values represent trend-based estimates.

LONG-TERM CHANGE (2016–2027)

| Area | 2016 | 2027 | Percentage Point Change | Relative Change |

| Cities | 13.4% | 9.1% | -4.3 | -32.1% |

| Towns and Suburbs | 10.3% | 7.1% | -3.2 | -31.1% |

| Rural Areas | 8.5% | 5.8% | -2.7 | -31.8% |

HOUSING AFFORDABILITY GAP IN 2027

| Location Type | Housing Cost Burden |

| Cities | 9.1% |

| Towns and Suburbs | 7.1% |

| Rural Areas | 5.8% |

City residents remain approximately 57% more likely to experience severe housing cost burdens than residents of rural areas.

KEY DRIVERS OF URBAN HOUSING PRESSURE

| Factor | Impact on Housing Costs |

| Population Growth | Increases housing demand |

| Urban Migration | Intensifies competition for housing |

| International Workforce Mobility | Raises rental demand |

| Limited Housing Supply | Supports higher prices and rents |

| Service Sector Expansion | Concentrates demand in major cities |

| Student Population Growth | Increases rental market pressure |

| Land Constraints | Restricts new development |

| Planning Delays | Slows housing delivery |

WHY RURAL AREAS REMAIN MORE AFFORDABLE

| Advantage | Effect |

| Lower Property Prices | Reduces ownership costs |

| Lower Rental Costs | Improves affordability |

| Greater Land Availability | Supports housing supply |

| Lower Population Density | Reduces demand pressure |

| Less Competition for Housing | Stabilizes prices |

| Remote and Hybrid Work | Expands residential options |

POLICY PRIORITIES ACROSS THE EUROPEAN UNION

| Policy Area | Objective |

| Affordable Housing Programs | Increase access to lower-cost housing |

| Residential Construction Expansion | Address housing shortages |

| Rent Stabilization Measures | Protect vulnerable households |

| First-Time Homebuyer Support | Improve homeownership opportunities |

| Urban Regeneration Projects | Increase housing stock in cities |

| Public Transport Investments | Connect affordable areas with employment centers |

| Planning Reform | Accelerate housing development |

| Social Housing Investment | Support lower-income households |

2027 EUROPEAN UNION HOUSING AFFORDABILITY SNAPSHOT

| Indicator | Value |

| City Housing Cost Burden | 9.1% |

| Town and Suburb Housing Cost Burden | 7.1% |

| Rural Housing Cost Burden | 5.8% |

| City-Rural Affordability Gap | 3.3 Percentage Points |

| Improvement in City Burden Since 2016 | 32.1% |

| Improvement in Rural Burden Since 2016 | 31.8% |

Related Report

* Global Housing Management Software Market Future Projections 2026-2033 * Global On-Demand Warehousing Market Overview and Outlook 2026-2033 * Global Digital Nomad Housing Market Revenue Forecasts 2026-2033 * Global Cold Chain Warehousing in Pharmaceutical Logistics Market Strategic Recommendations 2026-2033 * Global Warehousing in Pharmaceutical Logistics Market Growth Opportunities 2026-2033 * Global Terminal Tank Warehousing Service Market Risk Analysis 2026-2033 * Global Photovoltaic Inverter Housing Market Future Projections 2026-2033 * Global Aluminum Die-casting Battery Housing Market Historical Impact Review 2026-2033 * Global Filter Bag Housing Market Growth Drivers and Challenges 2026-2033 * Global SMC Composite Battery Housing Market Industry Best Practices 2026-2033 * Global Pharmaceuticals Temperature Controlled Warehousing Service Market Competitive Environment 2026-2033 * Global Logistics Warehousing System Market Competitive Environment 2026-2033 * Global Flight Electric Drive Housing Related Parts Market Technological Advancements 2026-2033 * Global Terminal Tank Warehousing Market Growth Opportunities 2026-2033 * Global Petrochemical Warehousing Market Key Success Factors 2026-2033 * Global Tank Warehousing Market Technological Advancements 2026-2033 * Global Logistics and Warehousing Software Market Risk Analysis 2026-2033 * Global Automotive Flywheel Housing Market Industry Best Practices 2026-2033 * Global Tank Warehousing Services Market Industry Best Practices 2026-2033 * Global Warehousing and Logistics Solutions Market Key Success Factors 2026-2033

최신 블로그

Parabolic Trough Collector Market Outlook Through 2035

Railway Propulsion Systems Market

Global Mental Health Outlook 2026-2030

The Next Five Years of Digital Innovation, AI Governance, and Europe's Competitive Future (2026

EU Digital Protection Index 2025: Public Confidence, Privacy and AI Governance

Public Concern About AI-Generated News Remains Limited Despite Rapid AI Adoption

Asia Gains Ground in Global Travel Demand: How the Global Tourism Map Is Being Redrawn Through

Housing Cost Burden in the EU Continues to Ease Through 2027, Yet Urban Residents Still Face th